Model your retirement at 50 in Breather

Enter your corpus, target age, city, and spend — and see a 20-year projection in minutes.

Fifty is the age most NRIs have circled for years. Real savings, kids wrapping up school, burnout at a peak — but retiring at 50 also means funding 35–40 years of retirement. Here is the real math.

Across every NRI community — Reddit's r/IndiaInvestments, WhatsApp groups, FIRE forums — age 50 comes up constantly as the target. And for good reason. By 50, many NRIs in the US, UK, or Canada have accumulated $500K–$1M+ in retirement accounts, home equity, and savings. Kids are often finishing high school or heading to college. The relentless US grind has worn thin. Family in India is getting older.

50 is old enough to have real capital. Young enough to still enjoy the move.

But here is the tension nobody talks about clearly: retiring at 50 means funding 35 to 40 years of retirement. That is not a planning detail — it fundamentally changes every number in the equation. The corpus that would be comfortable at 60 is dangerously thin at 50.

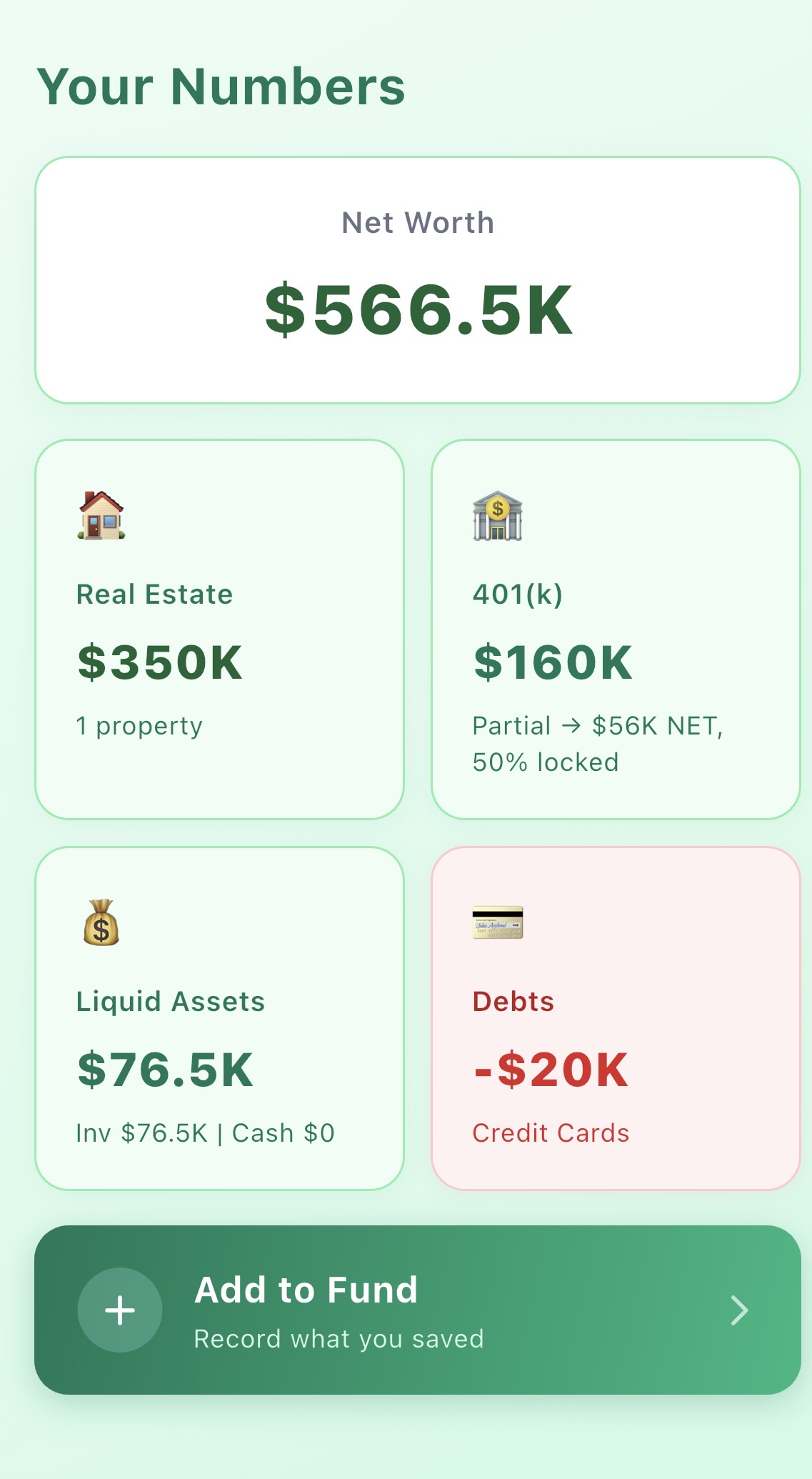

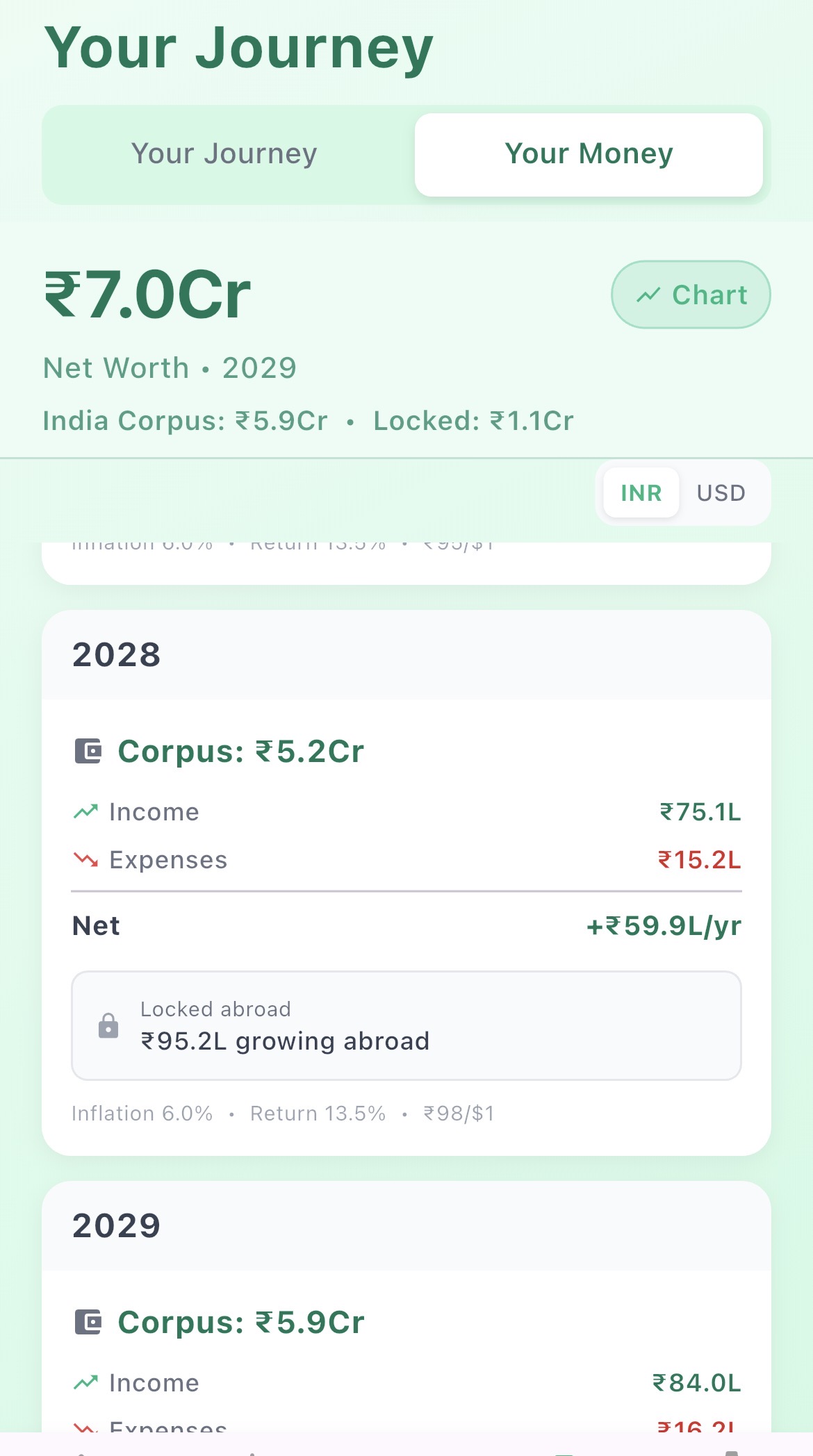

Most retirement calculators are built for 65-year-olds. Most "is X crore enough" posts on Reddit assume 25-year retirements. If you are targeting 50, you need to stress-test your plan against a much longer horizon — and the Breather retirement calculator is built specifically for this. Model your exact age, city, and spend before you make any decisions.

This guide walks through the real math: the inflation problem, the corpus numbers by city, three concrete dollar-amount scenarios, the passive income advantage, and a readiness checklist you can work through today.

Standard financial planning in India uses a 20–25 year retirement horizon. Trinity Study research (the basis of the 4% rule) was calibrated for 30 years. Neither of those fits someone retiring at 50 in India with a life expectancy pushing 85–90.

Here is why the extra decade matters so much:

Inflation compounds relentlessly. At India's historical 6% inflation rate:

That means the ₹1.5L/month lifestyle you are planning at 50 will cost ₹11.5L/month when you are 85. Your corpus must grow faster than that inflation curve for the entire duration — which rules out conservative FD-heavy portfolios. You need meaningful equity allocation even in retirement.

The safe withdrawal rate drops. The classic 4% rule was designed for 30-year retirements. For a 35-year retirement starting at 50, research suggests lowering this to 3.5–3.8%. In the Indian context — where equity markets have historically returned 10–12% and inflation runs at 6% — a 4% withdrawal rate is still workable if you maintain a 60–70% equity allocation. But it requires discipline and a willingness to adjust spending in down years.

The practical implication: Where a 60-year-old might use a 25× corpus multiple (annual expenses × 25), a 50-year-old should use 28–30×. That is a significant difference. Use the Breather calculator to see exactly how many years your specific corpus lasts at different withdrawal rates.

Also see our broader guide on how much money you need to retire in India for the full framework.

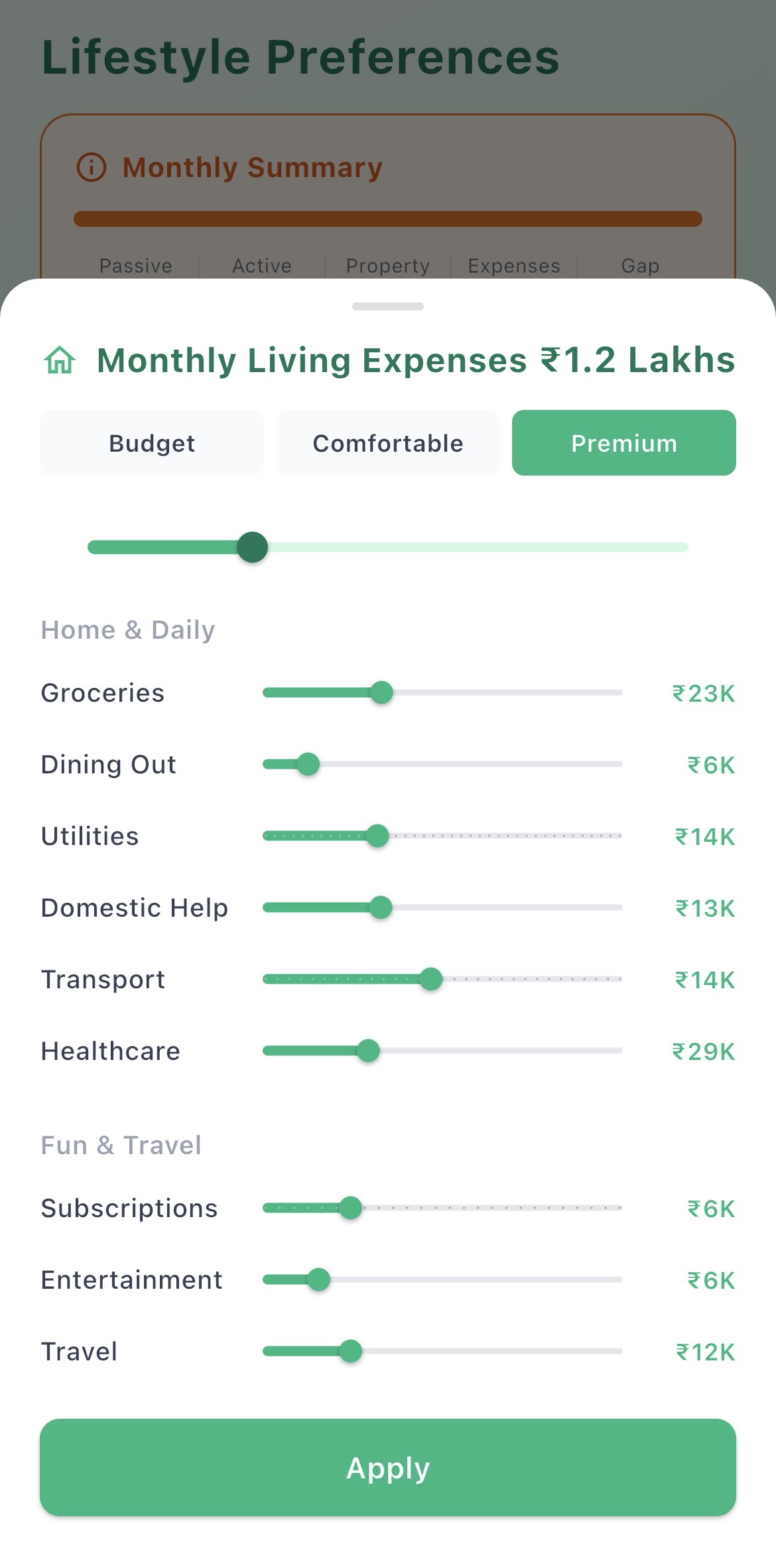

Your city is your single biggest financial decision. It determines 60–70% of your monthly spend. Mumbai costs nearly 2.8× what a Tier 2 city costs for a comparable NRI lifestyle. The table below shows what the numbers actually look like — using both a 25× multiplier (aggressive, for illustration) and the more appropriate 30× multiplier for age 50.

| City | Monthly Spend (NRI lifestyle) | Annual Spend | Corpus @ 25× | Corpus @ 30× (recommended at 50) |

|---|---|---|---|---|

| Mumbai | ₹2.5L | ₹30L | ₹7.5 Cr | ₹9 Cr |

| Bangalore | ₹2L | ₹24L | ₹6 Cr | ₹7.2 Cr |

| Hyderabad | ₹1.6L | ₹19.2L | ₹4.8 Cr | ₹5.76 Cr |

| Pune | ₹1.5L | ₹18L | ₹4.5 Cr | ₹5.4 Cr |

| Kochi | ₹1.2L | ₹14.4L | ₹3.6 Cr | ₹4.32 Cr |

| Tier 2 Hometown | ₹90K | ₹10.8L | ₹2.7 Cr | ₹3.24 Cr |

The 30× multiplier is the more appropriate benchmark if you are retiring at 50. The 25× figure assumes a shorter runway and tighter margins. Choosing Pune over Bangalore at age 50 means needing ₹1.8 Cr less corpus — that is roughly $220,000 USD at current exchange rates, which is a material difference.

For a detailed breakdown of which city is right for your situation — climate, healthcare, community, and real costs — see our complete city comparison guide.

Most NRIs think in dollars because that is what they earn and save. Here is what three realistic corpus levels actually deliver if you move at 50. These scenarios assume a 70% equity / 30% debt portfolio returning approximately 9% annually in India, against 6% inflation, with no other income sources. Run your own numbers in the Breather calculator.

Verdict: This works. Pune's cost of living gives enough headroom for $500K to last to the early 80s without passive income. It's tight but sustainable if you maintain discipline and don't lifestyle-inflate in the first decade. See our full $500K retirement in India analysis for deeper scenarios.

Verdict: Comfortable in a Bangalore-tier city. The withdrawal rate is conservative enough that the corpus actually grows in real terms through the 60s, giving you a strong buffer for healthcare costs or one-time expenses later. This is the sweet spot for many NRIs targeting metro living at 50.

Verdict: Excellent. At $1M and ₹2.5L/month, the corpus is growing significantly faster than you can spend it — even in a metro. This gives you full freedom of city, lifestyle flexibility, and a substantial inheritance or healthcare buffer. See our full $1 million retirement in India guide.

One thing that makes age 50 more achievable than the raw corpus numbers suggest: many NRIs at this stage have meaningful passive income streams that dramatically reduce the pressure on the corpus.

Common passive income sources for returning NRIs at 50:

Here is why even modest passive income changes the math dramatically:

If you can generate ₹50K/month in passive income, you effectively need ₹1.5–2 Cr less in your retirement corpus. That is a $175,000–$230,000 difference — or roughly 2–3 extra working years avoided. Model both scenarios (with and without passive income) in the Breather calculator to see the difference for your specific situation.

Before you book your one-way ticket, work through this checklist honestly. Each item represents a real planning gap that has derailed NRI returns.

For a comprehensive walkthrough of the financial planning process — RNOR status, NRE/NRO accounts, tax implications, and the India re-entry checklist — see our complete return-to-India financial planning guide. If you are moving from the US specifically, the moving back to India from USA guide covers the practical steps in detail.

Also worth reviewing: retiring in India from the USA — the full guide, and if you are thinking about whether your current savings are close to the target, check whether ₹5 crore is enough or whether ₹3 crore is enough for your situation.

Enter your corpus, target age, city, and spend — and see a 20-year projection in minutes.

Enter your corpus, city, and monthly spend — Breather shows a 20-year retirement projection. Free to start.