Run your ₹5 crore scenario in Breather

Enter your corpus, city, and spend — and see exactly how long your money lasts.

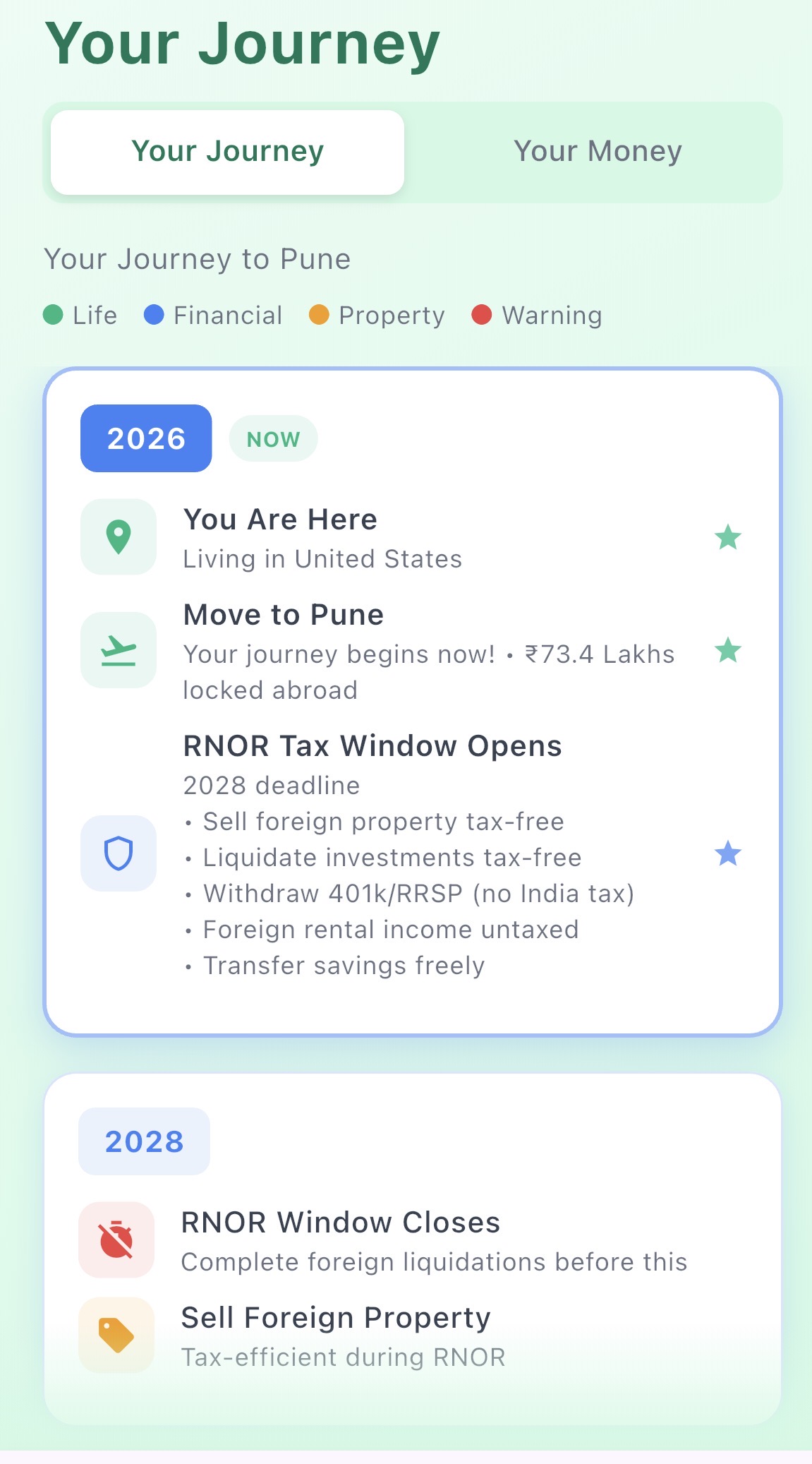

The short answer: it depends on your age, city, and family situation. Here are four real NRI scenarios that show exactly what ₹5 crore looks like over a 30-year retirement in India.

"Is ₹5 crore enough to retire in India?" appears on Reddit every week. It's searched thousands of times a month on Google. That's because ₹5 crore (~$600K USD) sits at the crossover point where many NRIs start seriously considering whether they can leave their foreign jobs and come home.

The answer isn't a yes or no — it's a function of four variables:

Here are four scenarios that map the full range of what ₹5 crore actually delivers in retirement in India, and how much you actually need based on your city and lifestyle.

This is the most optimistic case. Returning young to a lower-cost city with a lean lifestyle — and no school fees eating into the corpus.

Verdict: ₹5 crore is enough here. A lean lifestyle in a Tier 2 city keeps drawdown low and you'll still have a meaningful corpus in your 70s.

This is where ₹5 crore gets strained. Metro costs, private school fees, and a longer retirement horizon put real pressure on the numbers.

Verdict: ₹5 crore is not enough in this scenario. You'd need ₹8–10 Cr, a leaner lifestyle, or part-time consulting income to make the math work in a metro with young kids.

Returning at 50 changes the calculus significantly — shorter retirement horizon, kids closer to finished with school, and often more assets accumulated.

Verdict: ₹5 crore works well here. Returning at 50 with a reasonable lifestyle in a Tier 2 metro gives you a solid financial foundation. College costs are a one-time hit, not an ongoing drain.

Mumbai is India's most expensive city. Add an NRI-level lifestyle (clubs, international travel, good schools) and ₹5 crore gets under serious pressure fast.

From the four scenarios above, the pattern is clear. ₹5 crore is enough if:

₹5 crore is not enough if:

If you hold a larger corpus, see our breakdown of retiring in India with $1 million.

This is the part most people overlook. ₹5 crore today sounds like a lot. But at 6% inflation, the purchasing power of that ₹5 crore halves every 12 years.

This is why the corpus projection matters more than the starting number. You don't need ₹5 crore — you need ₹5 crore invested in assets that grow faster than inflation while you draw down on them.

Enter your corpus, city, and spend — and see exactly how long your money lasts.

See exactly how long your money lasts — based on your age, city, and lifestyle. Free to start.