Model your $1M scenario in Breather

Enter your savings, 401k details, city, and spend — and see exactly what your retirement looks like.

$1 million sounds like more than enough. But after 401k penalties, currency conversion, and 30 years of Indian inflation — the real answer is more nuanced. Here's the full breakdown.

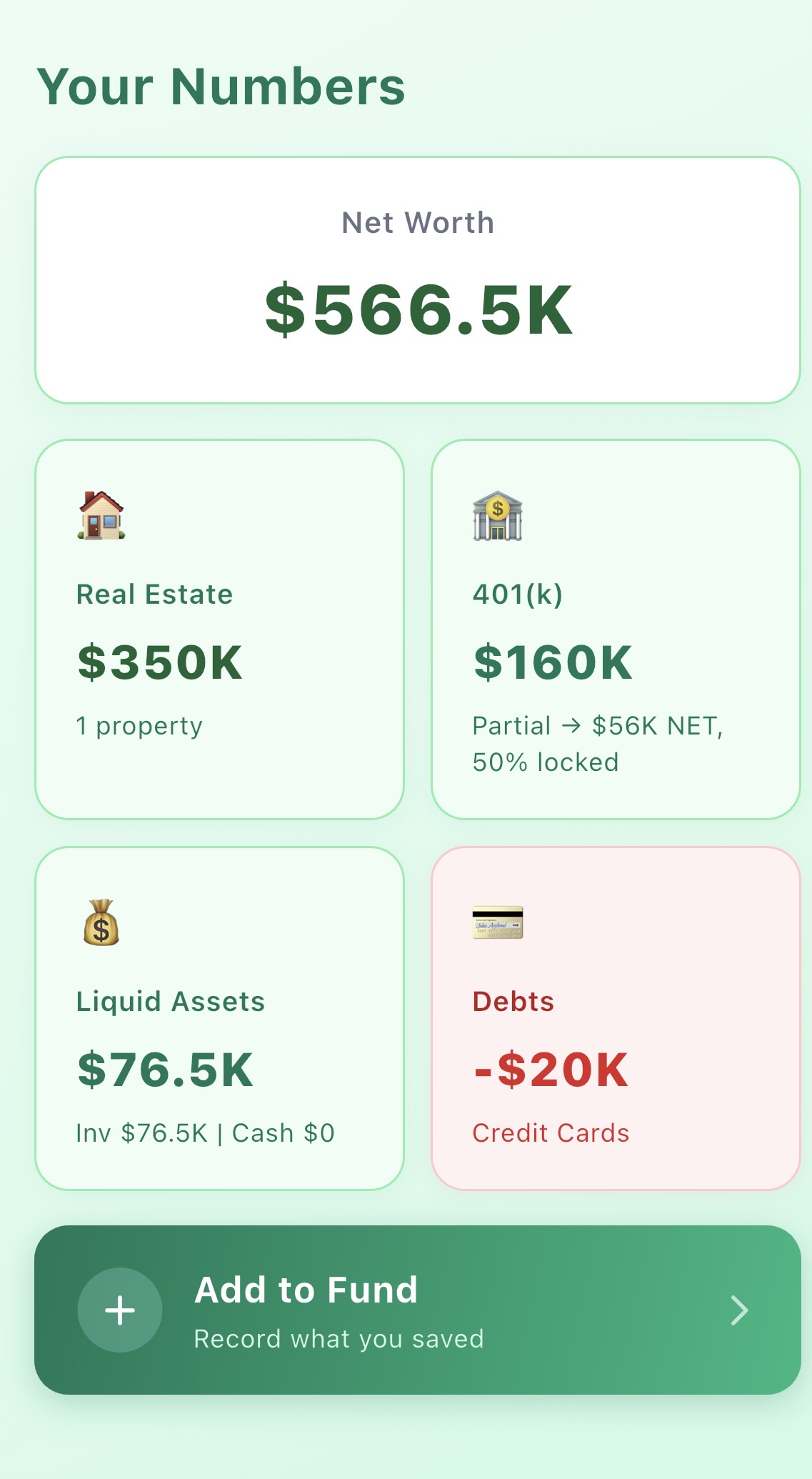

At current rates, $1 million converts to approximately ₹8.3 crore. That sounds like an enormous amount. And in India, it is. But there are three major reductions that happen before that money is actually available to fund your retirement:

If a significant portion of your $1M is in a 401k and you're under age 59½, withdrawing early costs you:

In a worst-case scenario, $400K in a 401k might net you only $240–260K after taxes and penalties. Your effective corpus shrinks significantly.

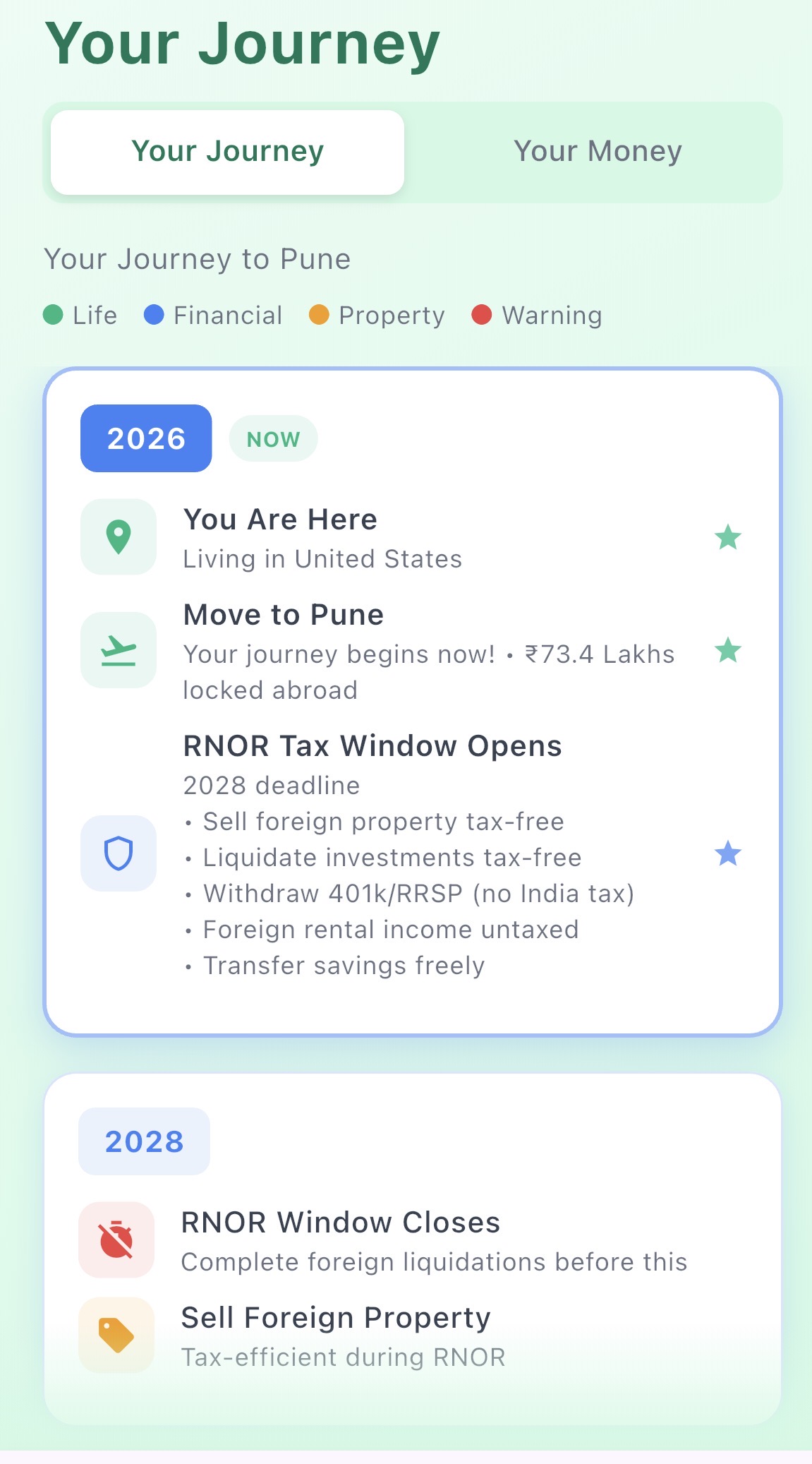

Even if your money converts at ₹83 today, the rupee has historically depreciated 3–4% per year against the dollar. Money you keep in US accounts gains value against the rupee over time — but money you convert and spend in India loses USD purchasing power every year.

India's lifestyle inflation runs 5–7% annually. Healthcare inflation is 10–12%. The ₹1.5L/month lifestyle you budget for at age 40 will cost ₹3L/month at age 55 in real terms.

This is the optimistic case. All funds are liquid (no 401k penalty), moderate lifestyle, Tier 2 city.

Verdict: Excellent outcome. $1M with no retirement account penalties in a mid-tier city is more than enough. You actually end up wealthier in absolute terms due to investment returns outpacing drawdown.

A more typical US NRI situation: most of the savings are in tax-advantaged accounts, and the family wants to live in a major city.

Verdict: $1M works, but it's not as comfortable as it sounds once you account for 401k penalties and metro costs. A part-time income stream would significantly improve the outcome.

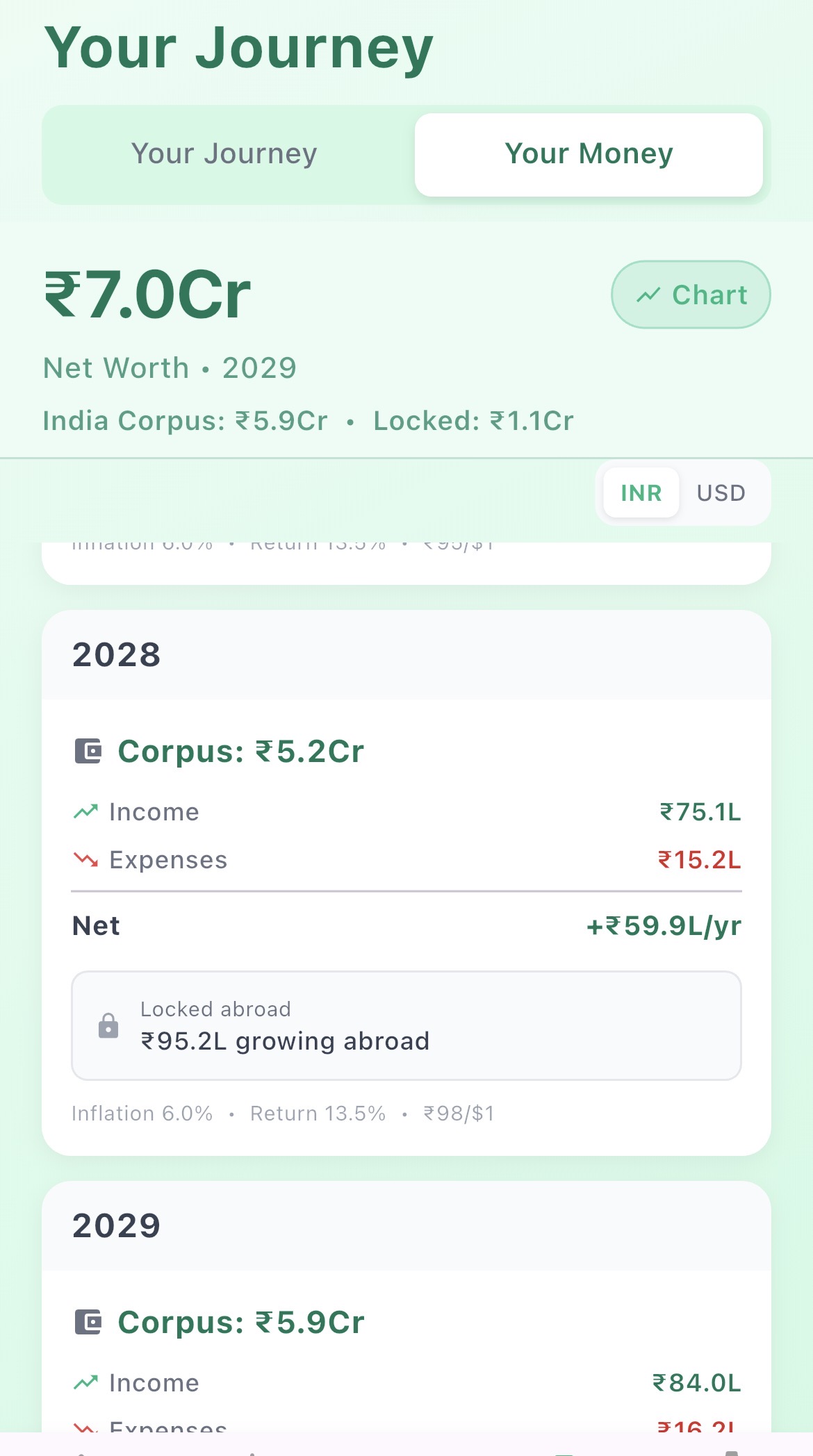

The smarter move: don't touch the 401k. Let it grow until 59½ penalty-free. Return to India with liquid savings only and keep the retirement account invested.

Verdict: The best strategy. Use liquid savings to fund the first 20 years in India. The 401k compounds untouched until 59½ — turning $600K into $2.4M+ at 7% growth. When it unlocks, you have an enormous second-phase corpus.

Based on these scenarios, here's a practical rule of thumb for NRIs thinking about retiring in India with $1 million:

If you're working with a smaller corpus, our ₹5 crore analysis runs the same scenarios at ~$600K.

To calibrate expectations: ₹8.3 Crore invested conservatively at 7% annual return generates about ₹4.8L/month in income. Most NRI couples planning an R2I spend ₹1.5–2.5L/month in Tier 2 cities. This means $1M — without touching principal — can cover most NRI lifestyles indefinitely.

The catch: inflation. That ₹1.8L/month lifestyle today costs ₹3.2L/month in 15 years at 6% inflation. Your investment return needs to outpace drawdown plus inflation — which is why a full financial plan matters more than a simple number.

Enter your savings, 401k details, city, and spend — and see exactly what your retirement looks like.

See exactly how your savings survive 20+ years in India — including 401k penalties, inflation, and city costs.