Plan your R2I finances in Breather

The only financial planning app built specifically for the NRI return to India decision.

The R2I decision involves more moving parts than any other financial planning scenario an NRI will face. This guide covers everything — currency risk, inflation, 401k strategy, healthcare, school fees, and property — so you know exactly what you're walking into.

Most FIRE planning assumes you're staying in the same country you earned in. Return to India financial planning is fundamentally different because you're crossing:

Each of these crossings has financial implications that compound over a 30-year retirement. Understanding them is the foundation of good return to India financial planning.

This is the most underestimated factor in return to India financial planning. The Indian rupee has depreciated against the US dollar by an average of 3–4% per year for decades.

What this means in practice:

The smart return to India financial planning strategy: don't convert everything at once. Keep your dollar-denominated assets invested and convert annually or as needed. You benefit from both USD investment growth and INR depreciation.

This illustrates why return to India financial planning should always consider the optimal currency conversion strategy — not just a one-time conversion.

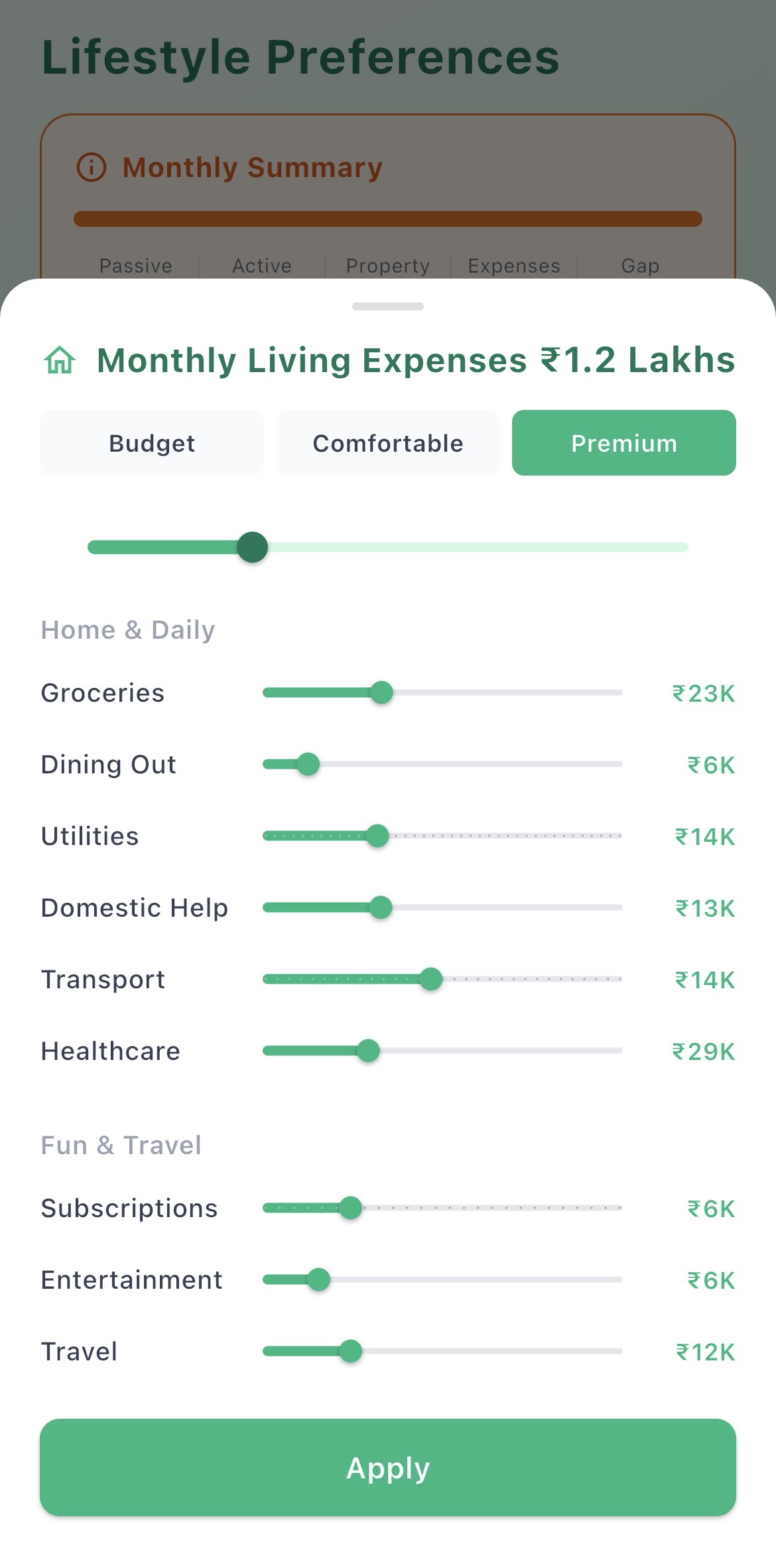

US NRIs are accustomed to 2–3% inflation. India runs at 5–7% for lifestyle expenses, and higher for specific categories:

At 6% inflation, your expenses double every 12 years. A ₹1.5L/month lifestyle at 40 costs ₹3L/month at 52, and ₹6L/month at 64. This is the most critical number in return to India financial planning — most people underestimate it severely.

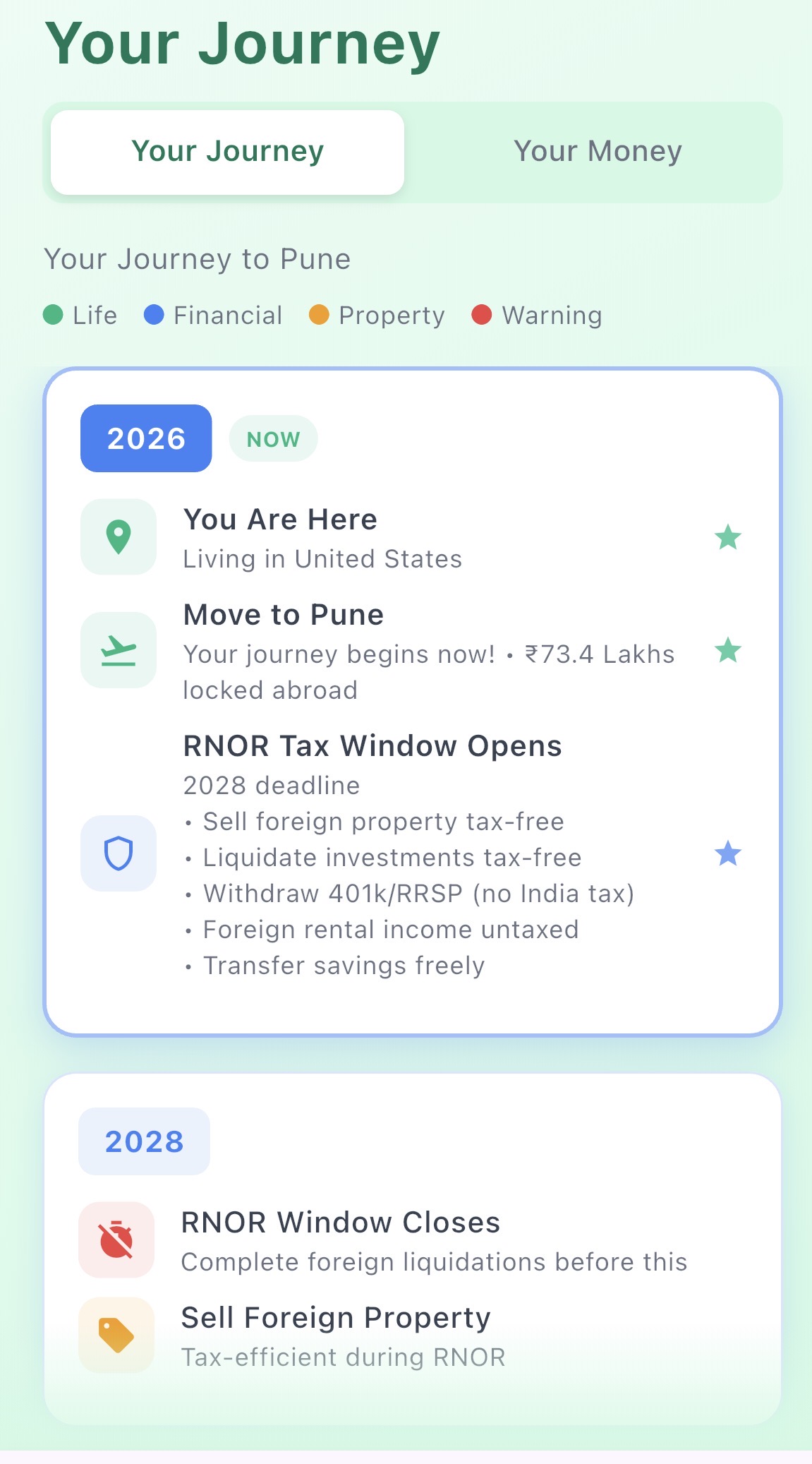

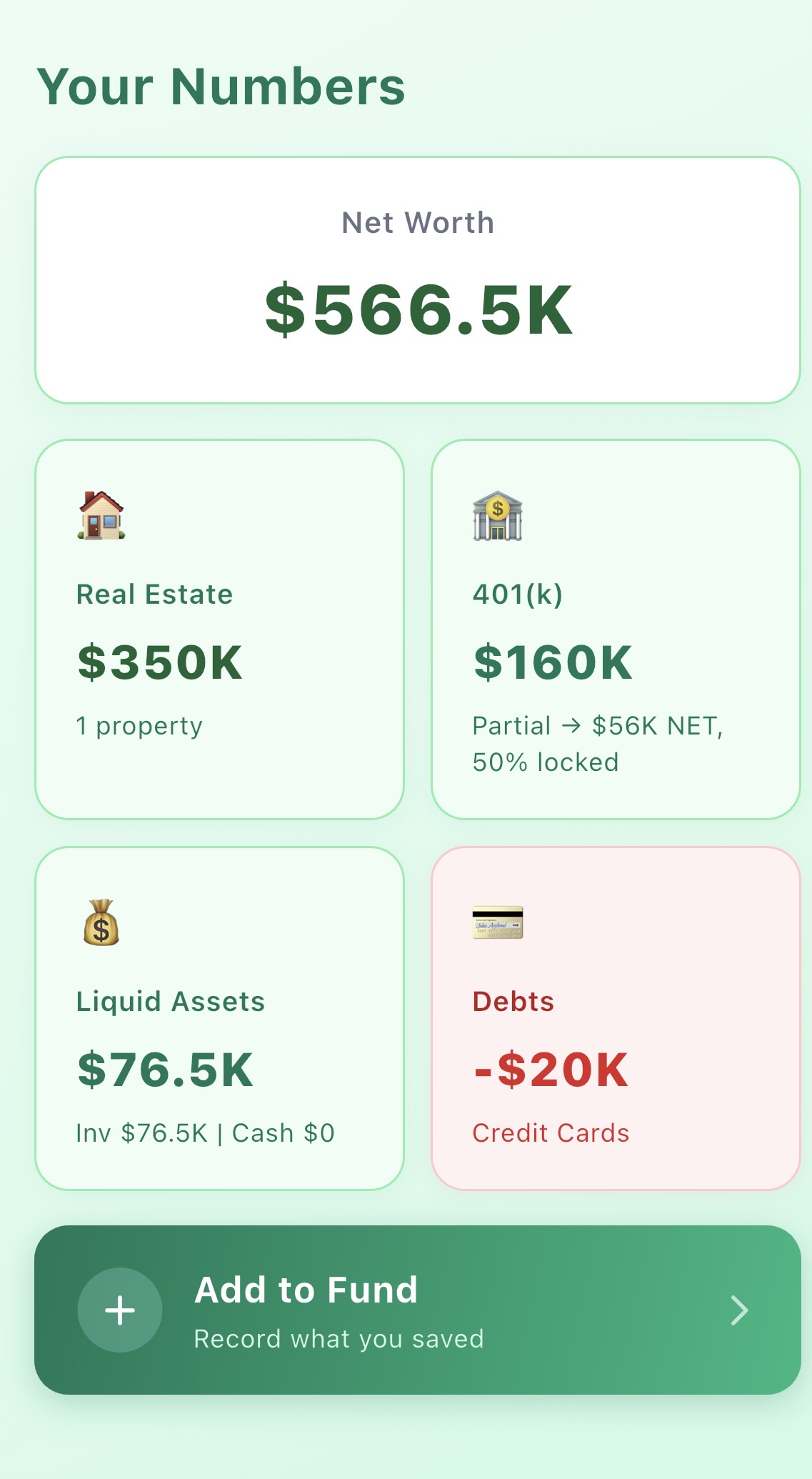

This is the biggest financial decision in your R2I plan, and the most commonly mishandled.

Withdrawing a US 401k before age 59½ costs:

Total effective loss: 30–45% of the withdrawal. On $400K, you might net $220–280K. This is a significant permanent loss of compounding capital.

Return to India with liquid savings only. Keep the 401k invested in the US. At 59½ you can withdraw without penalty — by which point a $400K 401k at age 40 might be worth $1.4M+ at 59½ (at 7% growth).

The return to India financial planning strategy that preserves the most wealth: use brokerage and savings accounts to fund the first 15–20 years in India, and let the 401k compound until you can access it penalty-free. If you're specifically moving from the US, our guide to retiring in India from the USA covers Social Security, FBAR/FATCA, Medicare gaps, and the exit tax in detail.

NRIs who return to India often assume healthcare is cheap. It is — until it isn't. Routine care is inexpensive. But major health events (cardiac surgery, cancer treatment, orthopaedic procedures) at premium hospitals in Indian metros cost ₹15–50L per event and are climbing fast.

Your return to India financial planning should include:

Budget: ₹20–35K/month in your 40s and 50s for insurance premiums + out-of-pocket. Rising to ₹50–80K/month in your 60s and beyond.

If you're returning with school-age children, education is the largest variable in your return to India financial planning. The range is enormous:

If you have two young children in international schools in Bangalore, you could be spending ₹40–50L per year on school fees alone. This is not compatible with a ₹5 Crore corpus.

The property question is central to return to India financial planning. Most NRIs face these choices:

The smartest return to India financial planning move for most NRIs: rent in India initially. Don't buy immediately. Spend 1–2 years understanding which city and neighbourhood actually suits your lifestyle before committing a significant portion of your corpus to India real estate.

The only financial planning app built specifically for the NRI return to India decision.

Download Breather — the only financial planning app built specifically for NRIs returning to India.