Plan your USA to India retirement in Breather

Enter your 401k split, liquid savings, city, and spend — and see your 20-year financial projection.

Retiring to India from the US involves far more than converting dollars to rupees. 401k penalties, Social Security timing, FBAR filings, Medicare gaps, and the India-US tax treaty all affect how much money you actually keep. Here's the complete financial roadmap.

NRIs returning from the UK, Canada, or Australia face complex tax situations — but the US has the most intricate web of rules. Three things make USA → India retirement uniquely complicated:

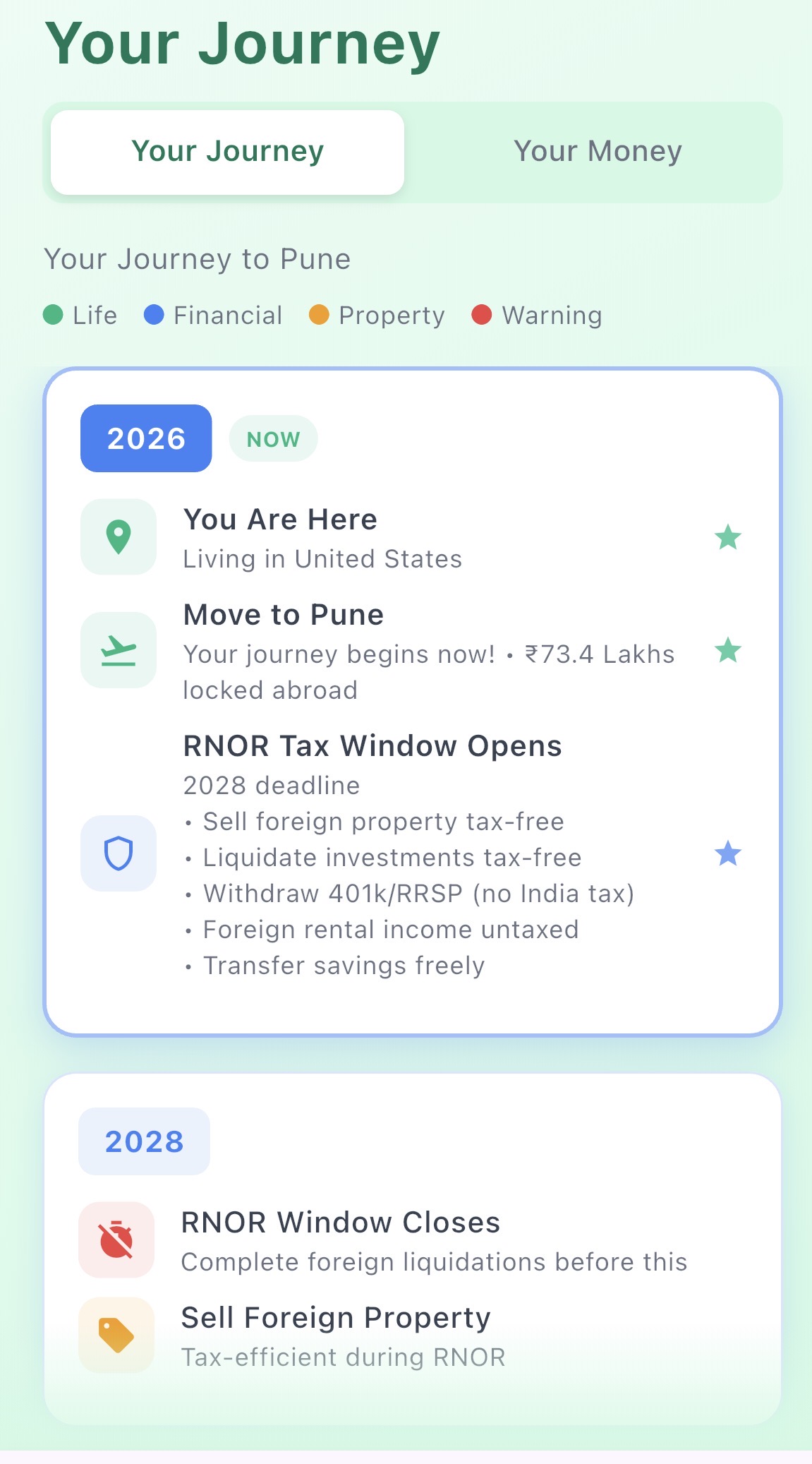

For a broader overview of the financial decisions involved in returning, see our complete return to India financial planning guide.

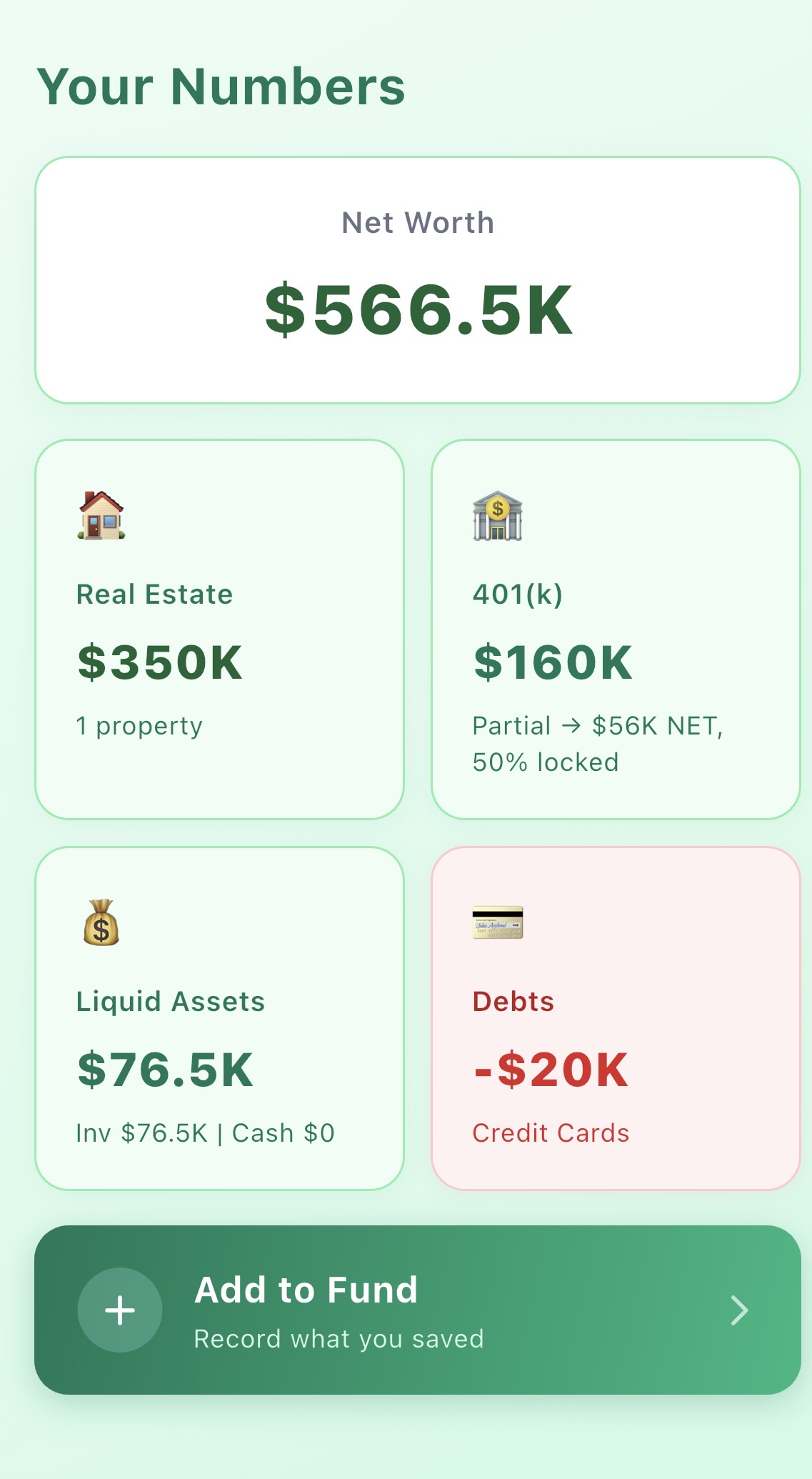

For most US-based NRIs, the 401k is the largest asset — and the most mismanaged in an R2I. Here are the four strategies, in order of financial efficiency:

Keep the 401k invested in the US, retire to India on liquid savings (brokerage, savings accounts), and start penalty-free distributions at 59½. The 401k compounds untouched for 10–20 years while you live in India. If you're 45 today and hold $400K in a 401k, it could be worth $1.1M by 59½ at 7% growth.

Convert traditional 401k/IRA funds to a Roth IRA gradually over several years before moving. You pay ordinary income tax on conversions — but in lower-income years, this can be tax-efficient. Roth withdrawals after 5 years are fully tax-free. Requires advance planning of 3–5 years before the move.

Rule 72(t) allows you to take "substantially equal periodic payments" from your 401k or IRA before 59½ without the 10% penalty. The catch: once you start, you must continue for 5 years or until 59½, whichever is longer. The distribution amount is calculated by IRS methods — not flexible.

If you need the cash now and none of the above applies, early withdrawal is the most expensive path. On $300K withdrawn at age 45 in the 24% tax bracket, you lose approximately $102,000 in taxes and penalties. Only consider this if your remaining corpus is large enough to absorb the hit.

Social Security benefits are paid to US citizens and permanent residents regardless of where they live — including India. Key points:

Medicare does not cover healthcare outside the United States. This is a critical gap for NRIs retiring to India in their 40s and 50s — years before Medicare eligibility (age 65).

What to do about the healthcare gap:

Once you're living in India and holding assets there, US reporting requirements kick in immediately. Missing these filings can result in severe penalties — $10,000+ per violation for non-willful FBAR failures.

Required annually if you have foreign financial accounts exceeding $10,000 in aggregate at any point during the year. This includes your Indian savings account, NRE/NRO accounts, mutual funds, and brokerage accounts. Filed separately from your tax return via the FinCEN website.

Required if foreign financial assets exceed $200,000 for single filers living abroad ($400,000 for joint) at year end, or $300,000 at any time during the year. Filed with your federal tax return (Form 1040).

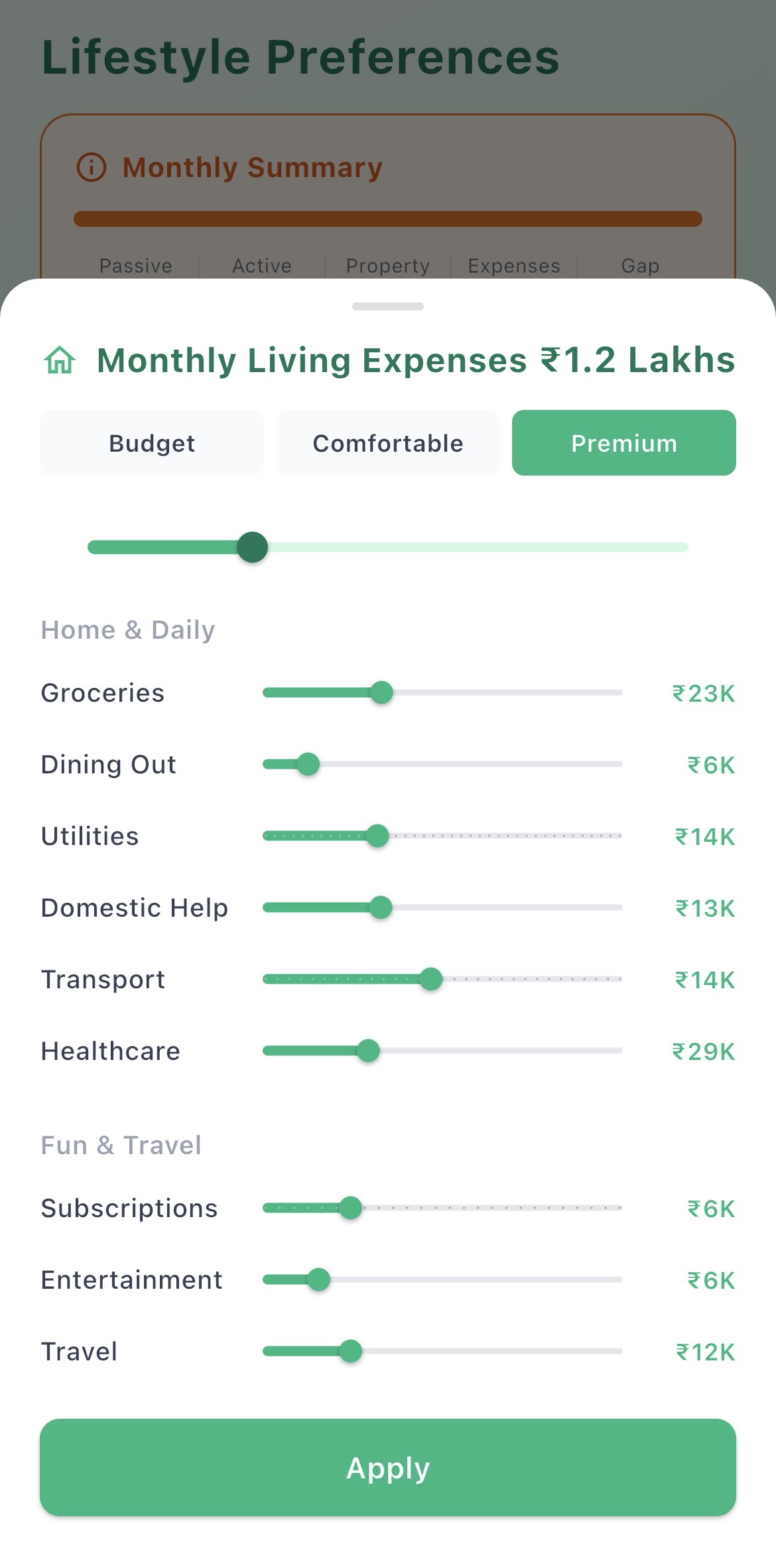

How and when you convert dollars to rupees can meaningfully impact your purchasing power over time:

For the full corpus analysis — how much you actually need — see our guide on how much money it takes to retire in India.

If you're a long-term US permanent resident (green card holder for 8+ of the last 15 years) and you surrender your green card, you may be subject to an "exit tax" under IRC Section 877A. This treats your worldwide assets as if they were sold on the day before expatriation — triggering capital gains tax on unrealized gains.

For US citizens, simply moving to India doesn't trigger exit tax — you remain a US citizen and continue filing US taxes. But if you're considering renouncing US citizenship (an extreme and largely irreversible step), the exit tax implications need to be evaluated carefully with a tax attorney.

Most NRIs returning to India keep their US citizenship or green card and simply become Indian residents for tax purposes — filing in both countries while claiming treaty protections to avoid double taxation.

Enter your 401k split, liquid savings, city, and spend — and see your 20-year financial projection.

Model your 401k, corpus, and city choice — and see exactly what your financial life looks like in India.