Model your ₹10 crore retirement in Breather

See exactly how your corpus grows or draws down — across different cities, spend levels, and investment strategies.

The short answer is almost always yes. But ₹10 crore at age 38 in Mumbai with a luxury lifestyle is a different story from ₹10 crore at age 45 in Pune with a moderate spend. Here's the real breakdown across four scenarios — and what ₹10 crore actually buys you in India.

₹10 crore (~$1.15M USD at ₹87/USD) is not a pipe dream for NRIs who've spent 15–20 years in the US tech sector, finance, or senior corporate roles. A software engineer at a large tech company who maxed their 401k, exercised RSUs, and invested consistently from their late 20s through mid-40s can absolutely arrive at this number.

Who typically reaches ₹10 crore before 50:

At this corpus level, the question fundamentally changes. You're no longer asking "can I retire?" You're asking "how do I retire well, and what does ₹10 crore buy me in India?" For context, compare with our $1 million retirement breakdown — ₹10 crore is roughly $1.15M, but the analysis diverges significantly because of India-specific investment options and lifestyle implications.

Start by running your scenario in the Retire in India Calculator — even at ₹10 crore, the city and age variables matter enough to warrant a proper projection.

Unlike ₹3 crore or ₹5 crore, which require careful scenario analysis and often come with significant constraints, ₹10 crore clears the retirement threshold in virtually all realistic NRI scenarios. The math is straightforward:

At a standard 4% withdrawal rate — the internationally accepted Safe Withdrawal Rate — ₹10 crore generates ₹40 lakh per year = ₹3.33 lakh per month in sustainable withdrawals. That is more than enough for a very comfortable life in any Indian city, including Mumbai or Bangalore at an elevated lifestyle level.

The 4% rule assumes your portfolio generates roughly 7–8% annually and inflation runs 3–4%. In India, where inflation averages 6–7% and equities have historically returned 12–14%, the sustainable withdrawal rate calculation is slightly different — but the principle holds. A ₹10 crore portfolio invested in a balanced Indian portfolio will generate more than enough for most NRI lifestyles, while maintaining or growing the principal.

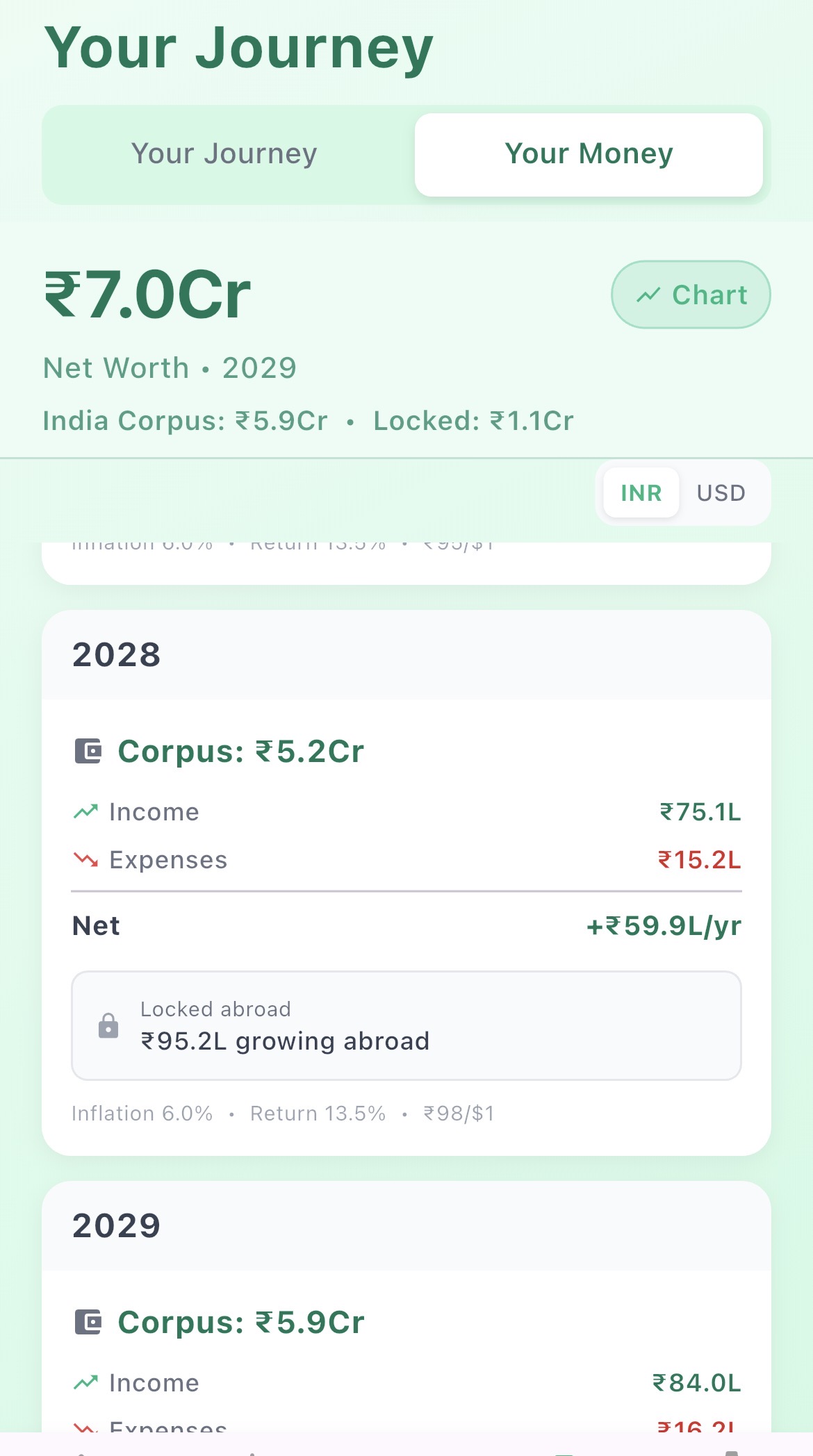

The interesting question at ₹10 crore is not survival — it's growth. How much will your corpus be worth in 20 or 30 years? In the best scenarios, you end up wealthier in absolute terms than when you started. Run the Retire in India Calculator with your exact age and spend to see your own projection.

Here's where the nuance lives. Even at ₹10 crore, the variables of age, city, and lifestyle produce dramatically different outcomes. These four scenarios map the realistic range.

Verdict: At ₹1.5L/month spend in Pune, you're withdrawing less than 2% of your corpus annually. Your investments compound far faster than your drawdown. You end up three times wealthier in absolute terms over 38 years. This is a genuinely exceptional outcome.

Verdict: Even with metro costs and private school fees, ₹10 crore at 45 in Bangalore grows strongly. The higher drawdown rate slows corpus growth, but investment returns still significantly outpace withdrawals. You end up nearly double your starting corpus at age 80.

Verdict: Sustainable but no longer growing significantly. With a ₹4L/month lifestyle in Mumbai including international school fees, you're drawing down principal over time. The corpus is still intact at 75, but the buffer is thinner. One major unexpected expense — a serious health event, a child's international education — needs to be planned for explicitly.

Verdict: The key insight: ₹10 crore is not unlimited. If you're returning at 38 or younger with a very high spend rate in a metro, you need to either reduce lifestyle expectations, plan supplemental income, or target a higher corpus. Use the Retire in India Calculator with your exact numbers to see where you fall.

At ₹10 crore, you have investment optionality that smaller corpora don't. You're not forced into conservative FD-heavy portfolios out of capital preservation anxiety. You have the cushion to take measured equity risk — and that makes an enormous difference over 30+ years.

India's long-run inflation averages around 6–7%. If your portfolio grows at 10%, your real return is approximately 3–4% — which is what the 4% rule is designed around. A portfolio that earns 10% while spending at 4% is sustainable essentially forever.

A 60/40 equity-debt split targeting 10% blended return against 6% inflation gives you a 4% real return — and at a 4% withdrawal rate from a ₹10 crore corpus, that's ₹40L/year that is fully sustainable in perpetuity.

The Breather app models different allocation strategies — FIRE-aggressive (higher equity, higher return target) vs Conservative (more debt, lower but more predictable return). Both scenarios update your corpus projection in real time. Use the Retire in India Calculator to compare them side-by-side for your specific situation.

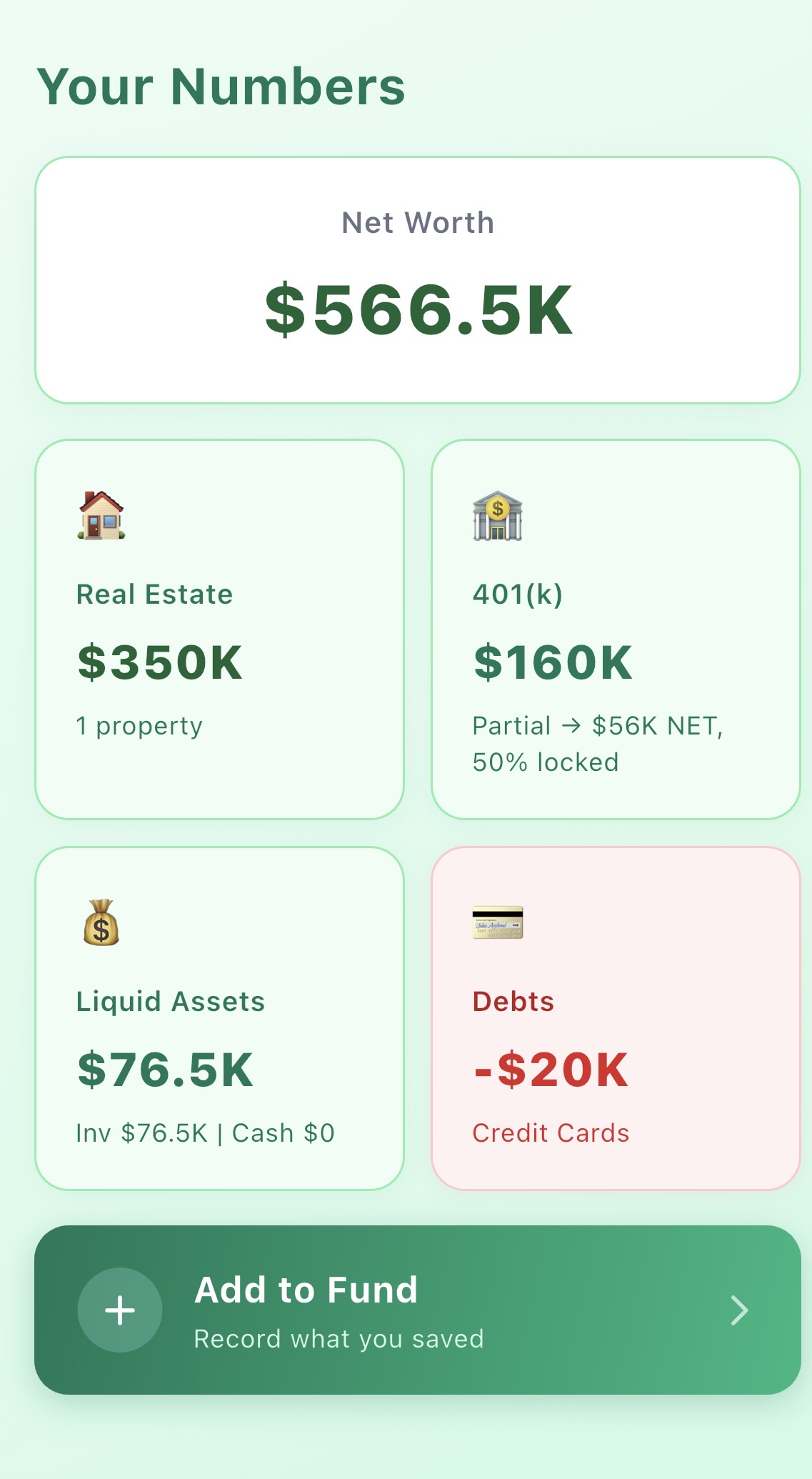

Let's make this concrete. What does ₹10 crore enable in India that smaller corpora don't?

At ₹10 crore, you can buy a genuinely premium apartment outright in most Indian cities — a 3BHK in a good Pune or Hyderabad locality, a 2BHK in Bandra or Koramangala without mortgage. Owning your home eliminates the single largest recurring expense in metros and permanently removes that line item from your monthly burn rate.

₹3.33L/month (the 4% SWR on ₹10 crore) comfortably funds international travel 1–2 times per year. A two-week Europe trip for a family of four, booked reasonably, runs ₹3–5L total. That's a single month's sustainable income — not a strain.

Premium corporate-equivalent health insurance in India costs ₹1–2L/year for a family of four with a generous cover. At ₹10 crore, this is 1–2% of annual income. You can also maintain a dedicated healthcare corpus of ₹50–75L in liquid investments for any large medical event — a joint replacement, a cardiac procedure — and still have ₹9.25–9.5 crore working for you.

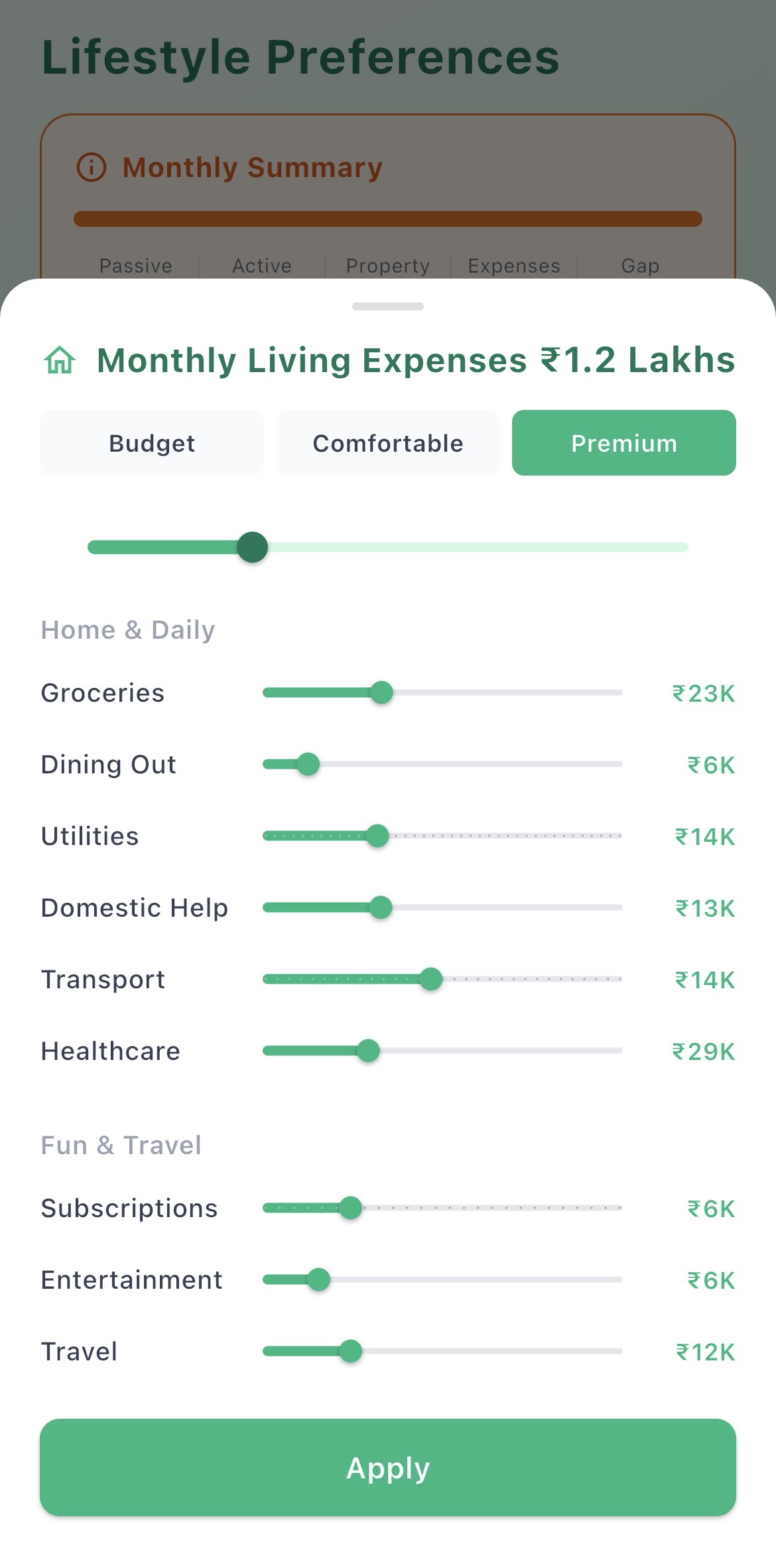

Premium private international schools in Bangalore or Pune charge ₹8–15L per year in fees. At ₹10 crore, that's 2–4 months of sustainable income per child per year — manageable, not crippling. Full-time domestic help (cook, driver, housekeeper) costs ₹30,000–60,000/month in metros — roughly 10–15% of your sustainable monthly income.

The overall picture: at ₹10 crore, you are genuinely in the top 0.1% of India in terms of financial security. You can live a lifestyle that most Indian professionals aspire to for decades — and your children inherit a substantial estate.

Numerically, ₹10 crore equals approximately $1.15M at today's ₹87/USD rate. Close to $1 million but not identical — and the distinction matters more than you think over a long time horizon.

The Indian rupee has historically depreciated roughly 3% per year against the US dollar. This means:

If you're holding your savings in USD and haven't converted yet, ₹10 crore is the floor, not the ceiling. Your $1M will likely be worth ₹11–12 crore by the time you retire in 5–7 years, purely from rupee depreciation.

The flip side: if you convert everything to INR the day you land and leave it all in Indian assets, you lose the natural hedge that USD holdings provide. A balanced approach — keep some USD assets, invest the rest in India — is usually optimal. This is especially important if you're still waiting for your 401k to vest or reach the 59½ threshold.

For a detailed USD-focused analysis, see Can You Retire in India With $1 Million. For a comprehensive look at what determines the right target corpus for your specific situation, How Much Money Do You Need to Retire in India covers the full framework. And if you're still building toward the ₹10 crore target and want to know what moving back looks like before you get there, Moving Back to India From the USA covers the financial mechanics of the transition itself.

See exactly how your corpus grows or draws down — across different cities, spend levels, and investment strategies.

Run your exact scenario in Breather — city, age, monthly spend, and investment strategy — and see the 20-year projection today.