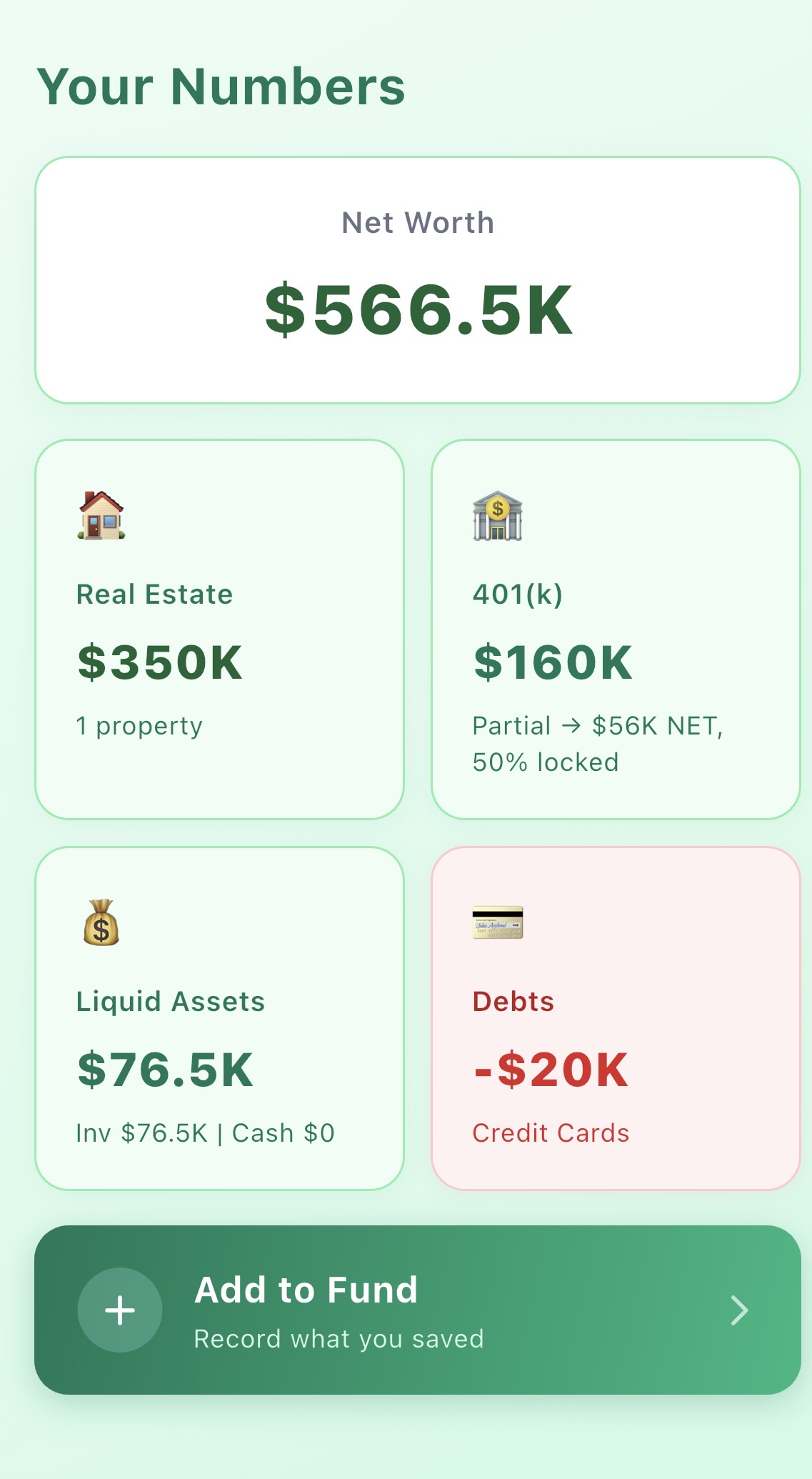

Model your ₹3 crore scenario in Breather

Enter your corpus, city, and spend — and see exactly how far your money goes.

₹3 crore (~$360K) is the corpus many NRIs hit first. The honest answer: it works only in specific circumstances — the right age, the right city, and a realistic lifestyle. Here are four scenarios that show the full picture.

Every few weeks, a new thread appears on r/IndiaInvestments or r/FIRE_Ind: "Is ₹3 crore enough to retire?" It's the first milestone most high-earning NRIs in their late 30s reach, and the answer genuinely depends on a few critical factors.

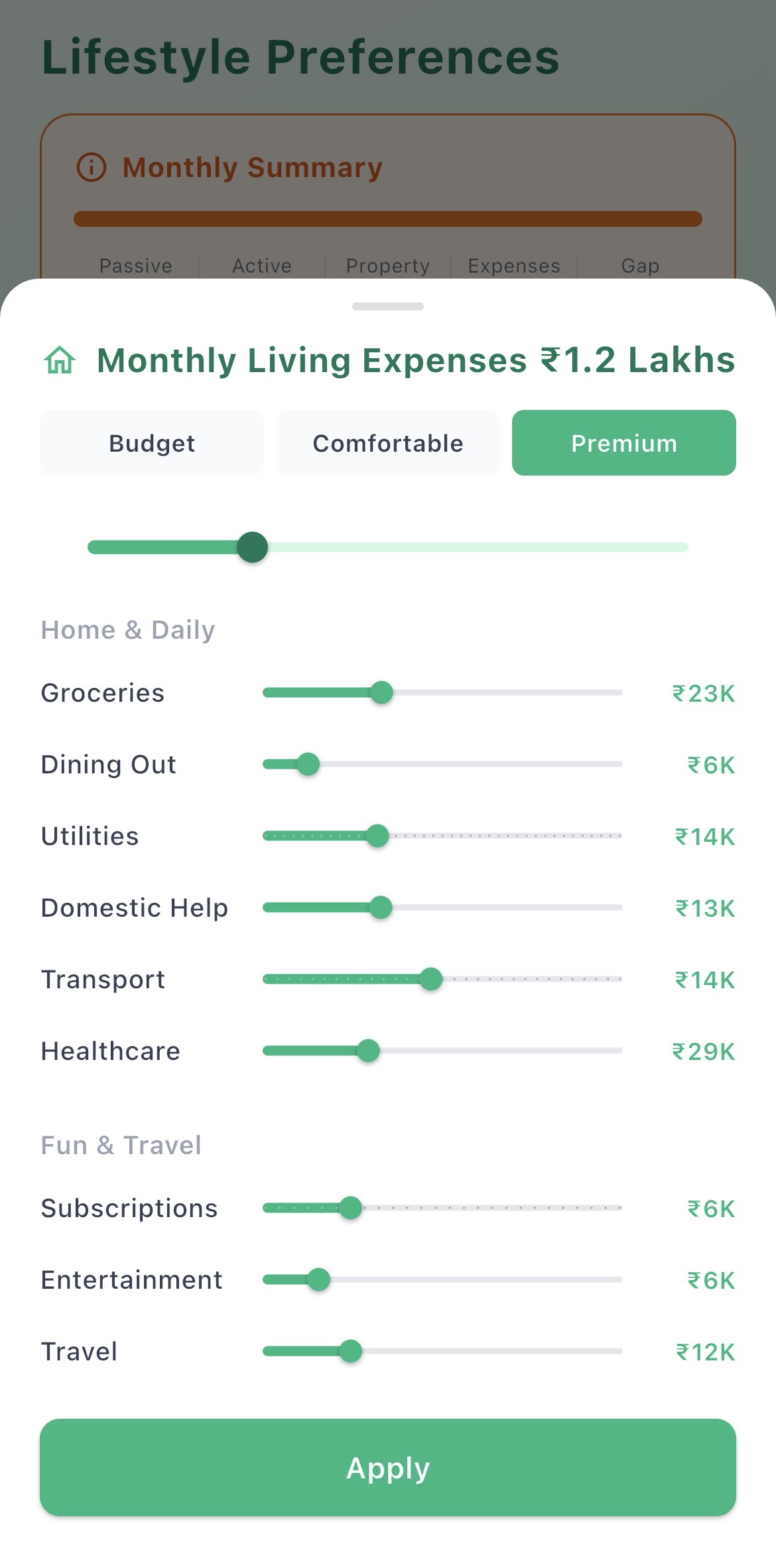

At 6% safe withdrawal, ₹3 crore generates roughly ₹1.5L/month. That sounds like a lot — until you factor in Indian inflation at 6–7% per year, healthcare costs rising at 10–12%, and school fees if you have young kids.

The four variables that determine whether ₹3 crore works:

For context on where ₹3 crore sits relative to other corpus sizes, see our full guide on how much you need to retire in India.

This is the scenario where ₹3 crore actually works. Returning later in life to a lower-cost city, with grown children and a settled lifestyle.

Verdict: ₹3 crore works here. A disciplined spend of ₹80K/month in a Tier 2 city, returning at 55, leaves a meaningful corpus 25 years out. It's lean but sustainable.

Returning a decade earlier adds significant pressure. School fees, a longer runway, and the need for a small buffer all strain ₹3 crore.

Verdict: ₹3 crore is not enough here without additional income. Either delay return until 50+, target a lower-cost city, or plan a consulting income stream before leaving your job.

This scenario shows how a modest rental income transforms the math. ₹25–30K/month in rental income from an inherited or owned property makes a huge difference.

Verdict: With rental income covering nearly a third of monthly spend, ₹3 crore becomes genuinely comfortable. The corpus is barely drawn down for the first decade, allowing investments to compound. This is the ₹3 crore success case for a 50-year-old.

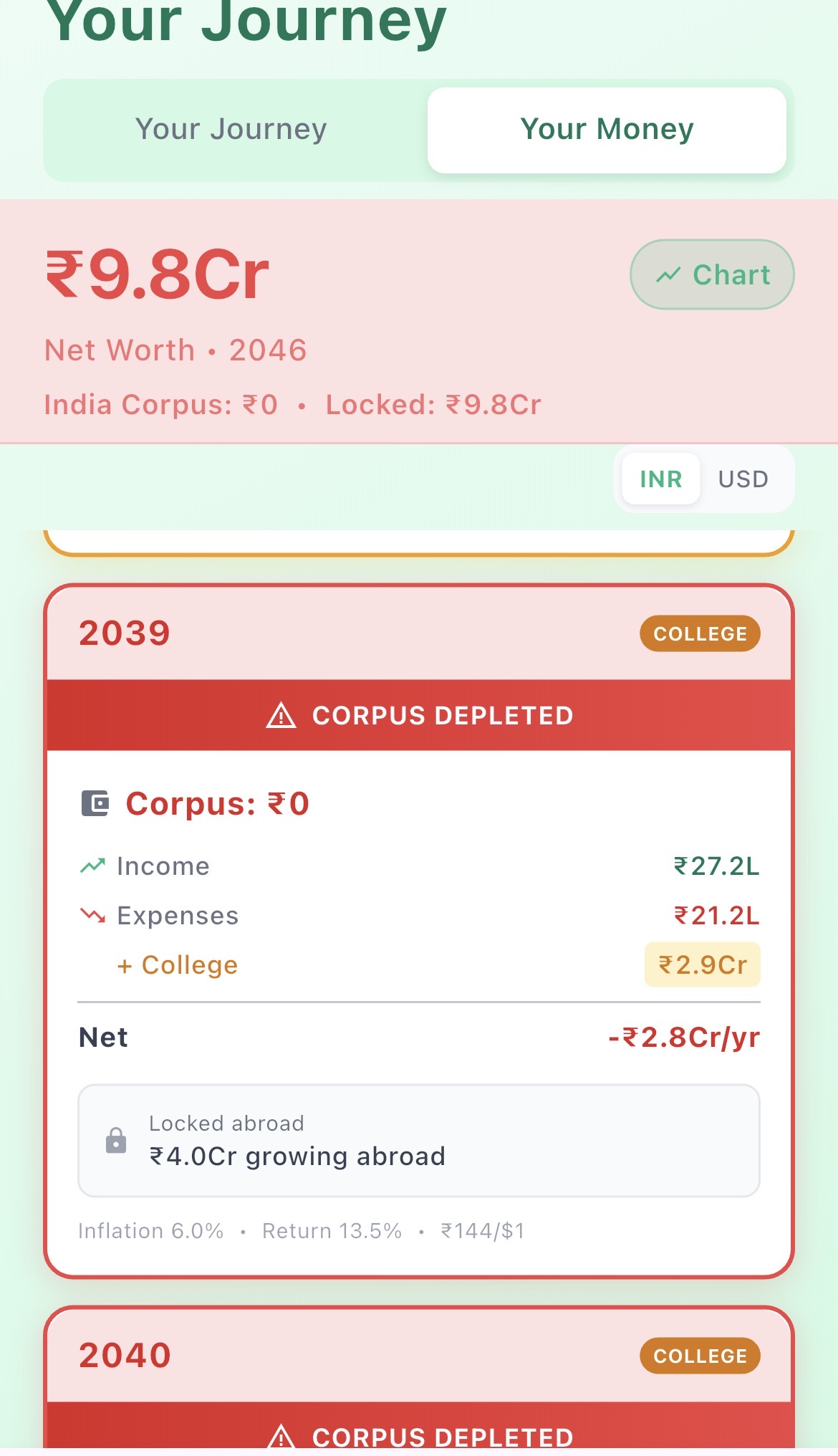

The worst-case scenario: returning young to an expensive metro with young children. ₹3 crore in this situation is dangerously thin.

Verdict: Do not attempt retirement in a metro with young kids on ₹3 crore. The math simply doesn't work, regardless of how you invest the corpus.

₹3 crore can work if:

₹3 crore is not enough if:

If you're close to ₹3 crore and wondering whether to wait, see what a ₹5 crore corpus looks like — the difference in outcomes is significant. The Breather app can run your specific numbers and show you the exact gap.

At 6% inflation, ₹3 crore today has the same purchasing power as ₹1.5 crore in 12 years. That's the core challenge: you need your investments to grow faster than inflation while you draw down expenses each month.

A conservative 7% return on a diversified portfolio means you can draw around ₹1.4–1.5L/month before principal erosion — but only before inflation catches up. In real terms, by year 15, you'll need more than ₹2L/month for the same lifestyle. Plan for this from day one.

Enter your corpus, city, and spend — and see exactly how far your money goes.

See exactly how long your money lasts — based on your age, city, and lifestyle. Free to start.