Model your $500K scenario in Breather

Enter your savings, 401k split, city, and spend — see your 20-year projection in minutes.

$500,000 converts to roughly ₹4.2 crore. It's half of the $1 million benchmark — but does it cut the viability in half too? Here are four real scenarios that show where $500K works, and where it doesn't.

At current rates, $500,000 converts to approximately ₹4.2 crore. That's more than many Indians earn in a lifetime — but for an NRI planning a 30–35 year retirement, the math is tighter than it sounds.

Unlike $1 million, $500K leaves very little room for error. Three things will define whether it works:

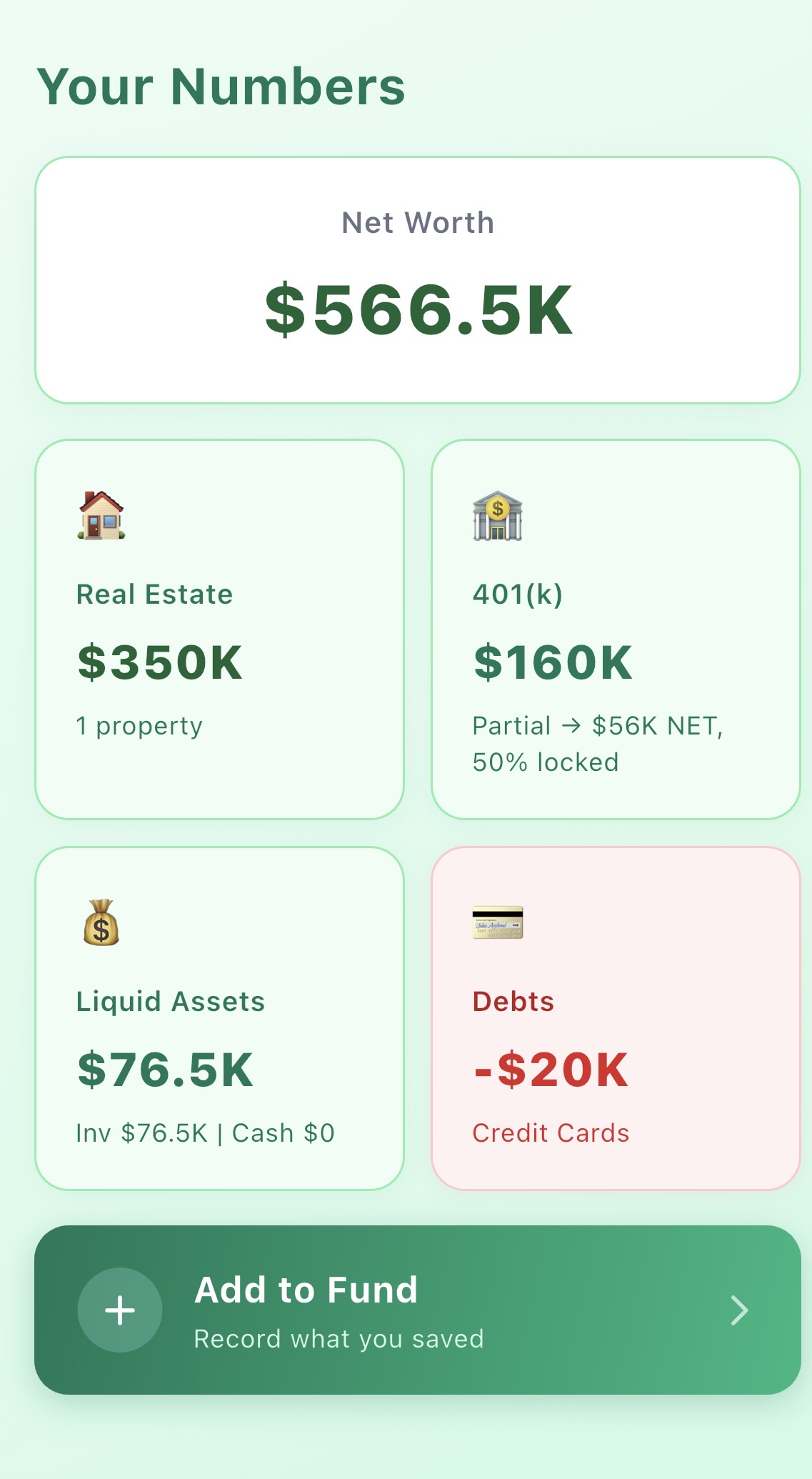

If half your savings are in a 401k and you withdraw early (before 59½), you lose 30–40% to federal taxes and the 10% penalty. On $250K in a 401k, that's $75–100K gone before the money even arrives in India. Your effective corpus drops to ₹3.0–3.4 crore — a fundamentally different starting point.

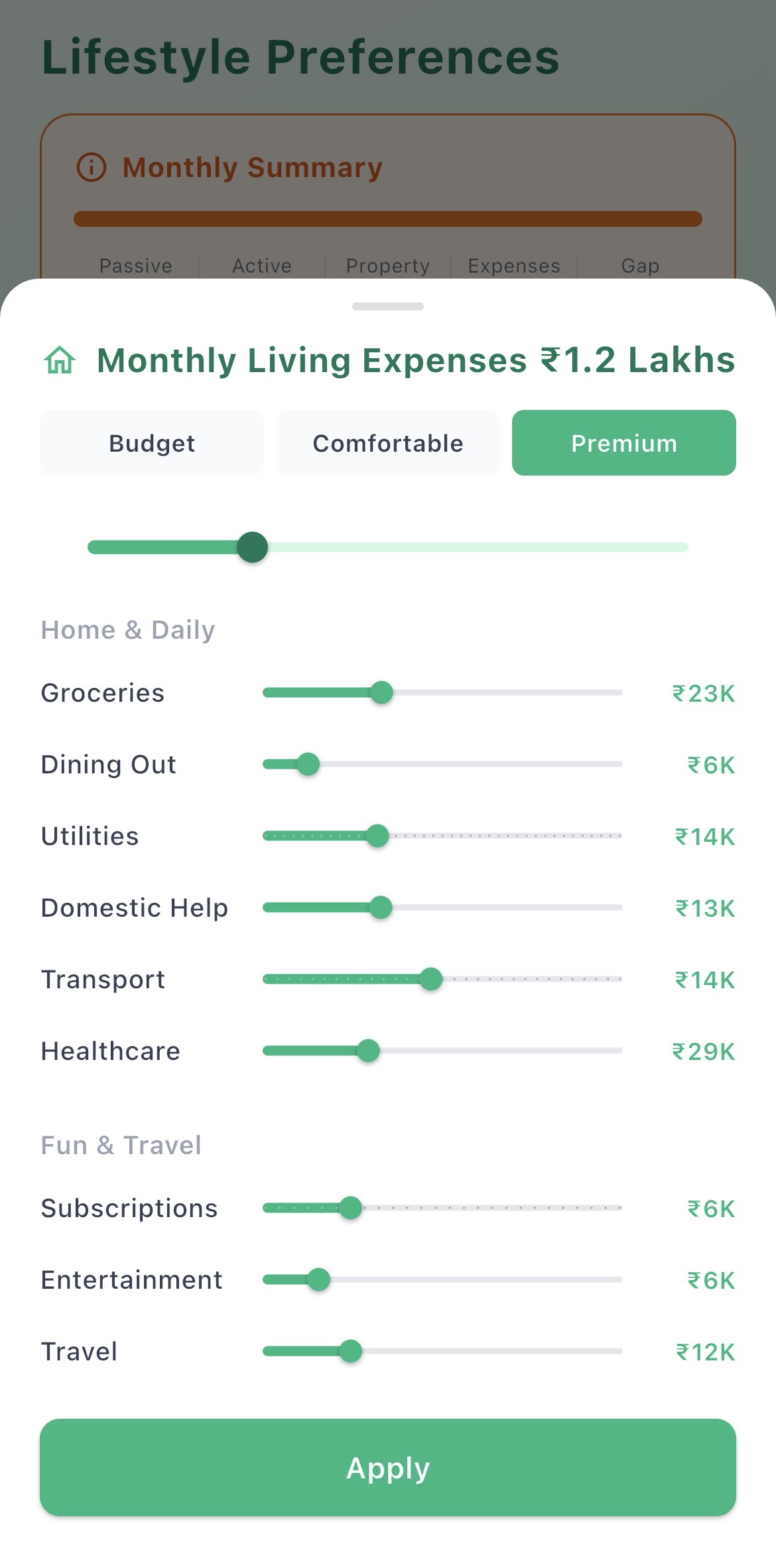

With $1M, your investment returns can outpace your drawdown for the first 10–15 years. With $500K, you're much closer to the edge where inflation and spending erode the corpus faster than returns rebuild it. City choice and spend discipline are non-negotiable.

A major medical event, a child's college abroad, or a home renovation can cost ₹30–80L. On a ₹4.2 crore corpus, that's a 7–19% hit. These are plan-breaking risks without a buffer strategy.

The most viable $500K scenario. Returning at 50 with a shorter runway, settled lifestyle, and a Tier 2 city significantly reduces the math pressure.

Verdict: $500K works here. A disciplined ₹90K/month spend in a Tier 2 city, returning at 50 with no 401k penalty, leaves a meaningful cushion at 80. It's lean but the math holds.

A common US NRI scenario: most savings in tax-advantaged accounts, mid-40s return, one child still in school. The 401k penalty alone changes the picture significantly.

Verdict: $500K with significant 401k exposure at 45 is not enough. Either delay the move, grow the corpus to $700–800K, or find a way to avoid the early 401k penalty.

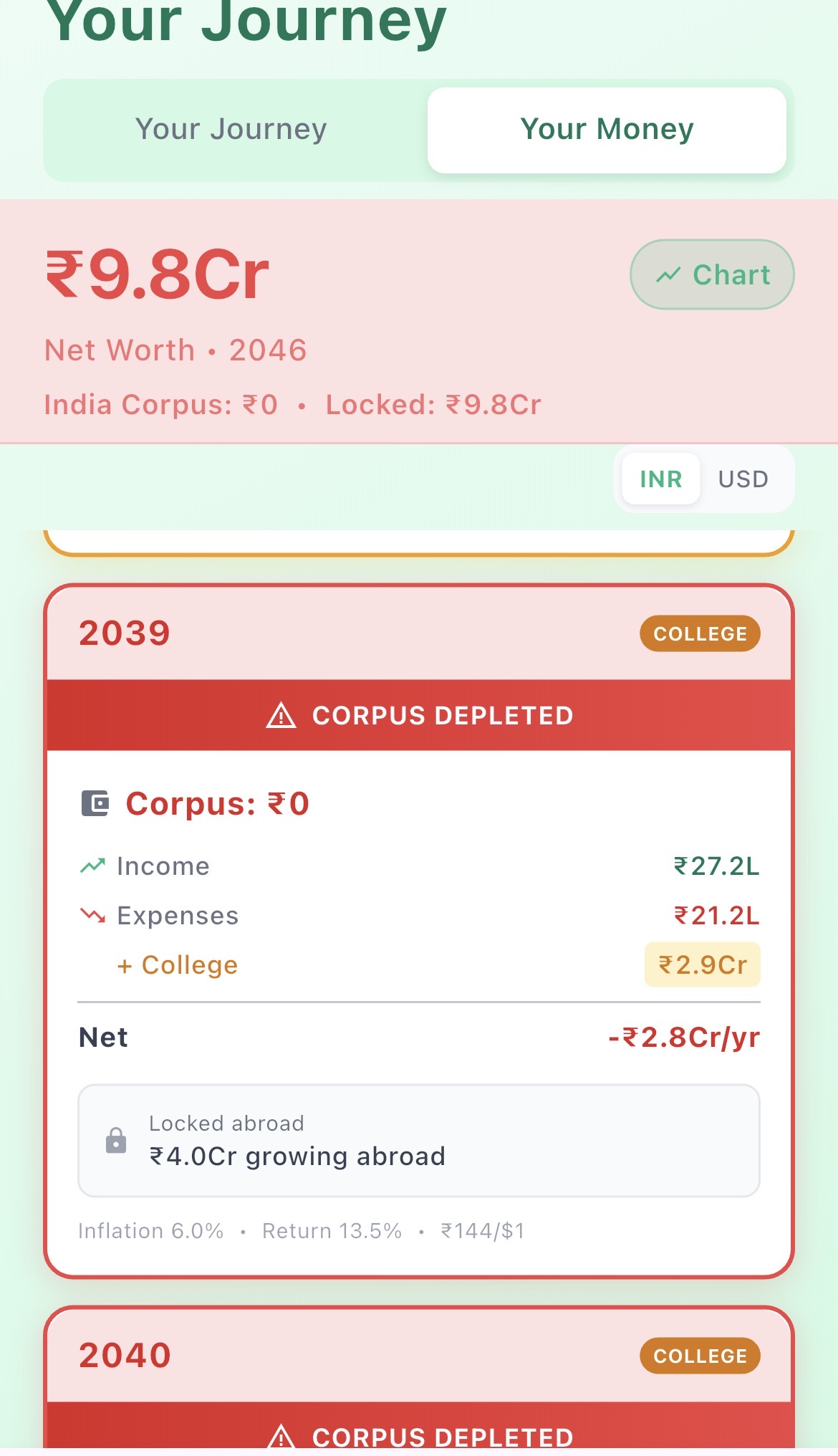

The smartest $500K move: keep the 401k invested, retire to India on liquid savings only, and unlock the 401k penalty-free at 59½.

Verdict: The $300K 401k held for 11 years at 7% growth doubles to $620K+. Combined with the liquid portion carefully drawn down, this is the best way to make $500K work. The 11 years of 401k compounding saves the plan.

The scenario where $500K clearly fails. Metro costs, young kids, and a 40-year runway are incompatible with a $500K corpus.

Based on these scenarios, here's the honest framework for deciding if $500K is enough:

If you have or are approaching $1M, see how the math changes with double the corpus — the additional flexibility is substantial.

Enter your savings, 401k split, city, and spend — see your 20-year projection in minutes.

See how far your savings go — including 401k penalties, Indian inflation, and city costs. Free to start.