Model your UK-to-India retirement in Breather

Enter your GBP savings, UK pension income, city preference, and target spend — and see your full retirement projection.

GBP goes remarkably far in India, and the UK State Pension is payable for life wherever you live — including Pune, Bangalore, or Kochi. But most British NRIs still get the corpus math wrong. Here's the complete picture for UK-based NRIs planning their India retirement.

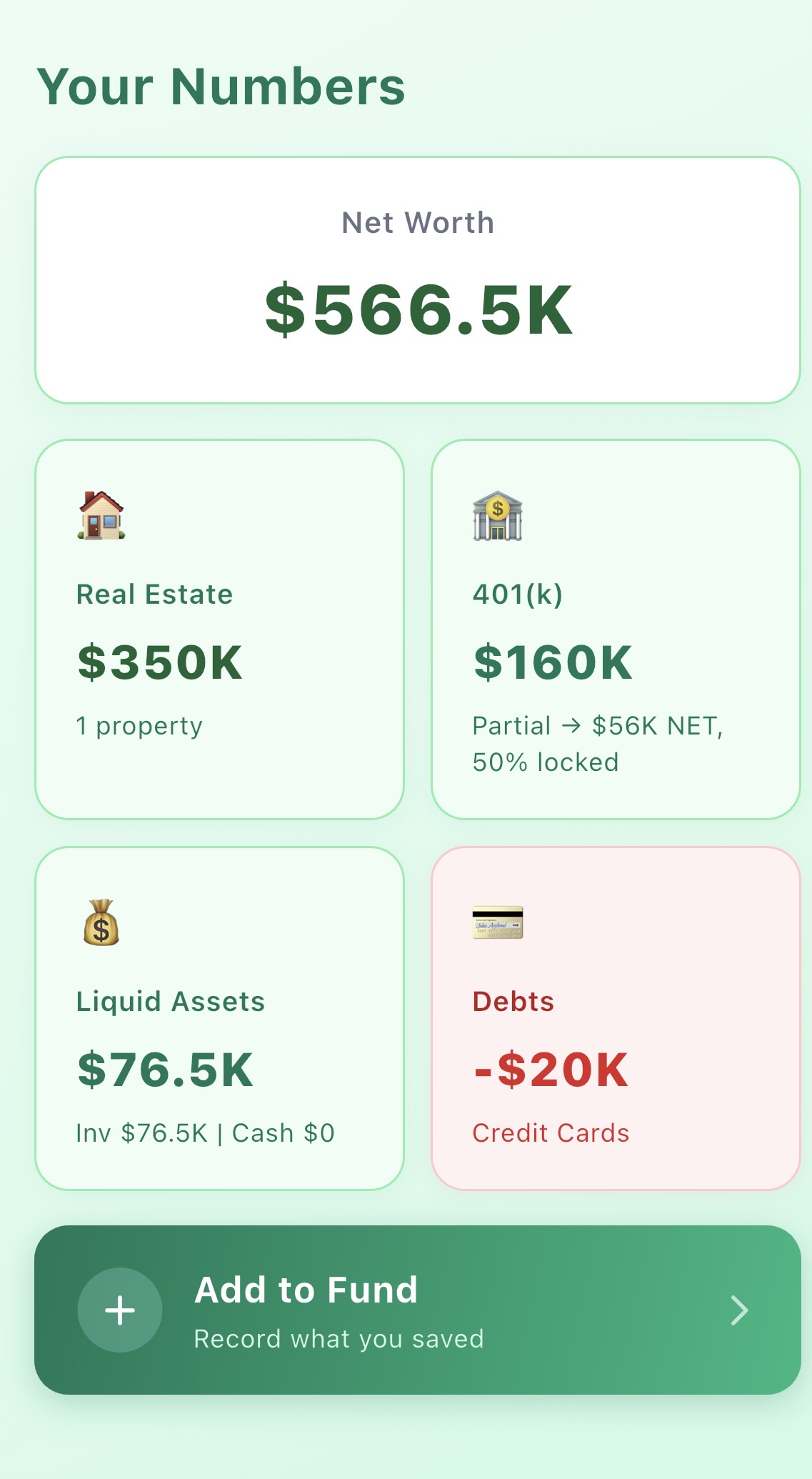

The exchange rate is one of the most compelling arguments for UK NRIs retiring to India. At roughly £1 = ₹110, a pound buys significantly more comfort in India than almost anywhere else a British NRI might retire. A £400,000 corpus converts to approximately ₹4.4 Crore — enough to fund a genuinely comfortable retirement in most Indian cities.

The catch is that many British NRIs look at the UK median pension pot — around £107,000 — and assume that's the benchmark. At £107K, you're looking at roughly ₹1.2 Crore, which is not enough to retire comfortably anywhere in India, even with a frugal lifestyle. That figure represents a meaningful gap for anyone planning an India retirement without a private savings cushion on top.

The picture is much better for NRIs who've spent careers in UK tech, finance, healthcare, or professional services. These individuals often have £300,000–£700,000 in total retirement savings — ISAs, SIPPs, workplace pensions, and liquid investments combined. At those numbers, the UK-India retirement math starts to look very attractive. Use the Retire in India Calculator to plug in your specific GBP corpus and see your projected monthly spend and corpus runway.

The key variables that determine whether your UK savings are enough:

For a broader view of what different corpus sizes deliver in India, see our guide on how much money you need to retire in India.

This is the question most UK NRIs don't ask early enough — and the answer is genuinely good news. The UK State Pension is payable worldwide, including India. If you've built up 35 qualifying National Insurance (NI) years, you receive the full new State Pension: currently £11,502 per year (approximately ₹1,26,500/year, or just over ₹10,500/month).

If you have between 10 and 34 qualifying NI years, you receive a proportional State Pension. Ten years is the minimum to receive anything at all. NRIs who spent 15–20 years in the UK before returning to India may qualify for a partial pension of £3,000–£7,000/year — still meaningful, still paid to you in India for life.

A few critical points about UK State Pension and India:

Beyond the State Pension, consider your workplace pension arrangements. Defined Benefit (DB) pensions from employers pay a guaranteed income for life — these remain in the UK and pay regardless of where you live. SIPPs (Self-Invested Personal Pensions) give you investment control and flexible drawdown from age 57 (rising to 57 from 2028). Both are payable while living in India.

The combination of UK State Pension plus a modest SIPP or DB pension can give many UK NRIs ₹1,50,000–₹2,00,000/month in guaranteed lifetime income — potentially enough to retire comfortably in a Tier 2 Indian city without touching savings. Run your specific numbers in the Retire in India Calculator to see what this means for your corpus requirement.

QROPS (Qualifying Recognised Overseas Pension Scheme) is a mechanism that allows UK pension holders to transfer their pension funds to a qualifying overseas pension scheme. The idea sounds appealing — bring your UK pension pot to India, invest in Indian assets, avoid UK tax complexity. The reality is more nuanced.

To transfer to a QROPS, the overseas scheme must be on HMRC's approved list and meet specific regulatory requirements. India has very limited QROPS-eligible schemes, which already narrows your options considerably. The transfer itself is possible for personal pensions (SIPPs) and some workplace defined contribution pensions, but defined benefit (DB/final salary) pensions are rarely worth transferring out of.

Since 2017, HMRC applies a 25% Overseas Transfer Charge (OTC) on transfers to QROPS unless you are resident in the country where the QROPS is based at the time of transfer. This means a UK NRI who transfers their £400,000 SIPP to a QROPS after moving to India would owe £100,000 in transfer charges — eliminating a quarter of their retirement savings immediately. This is a very large cost that most people underestimate.

For the vast majority of UK NRIs retiring to India, the better strategy is to keep UK pensions in UK-based schemes and draw them as income while living in India. This avoids the 25% transfer charge, keeps your funds in GBP (which historically appreciates against INR), and maintains UK regulatory protections. The drawdown income is then transferred to your Indian NRE account as needed.

For the full picture of financial planning considerations when moving back, read our Return to India financial planning guide.

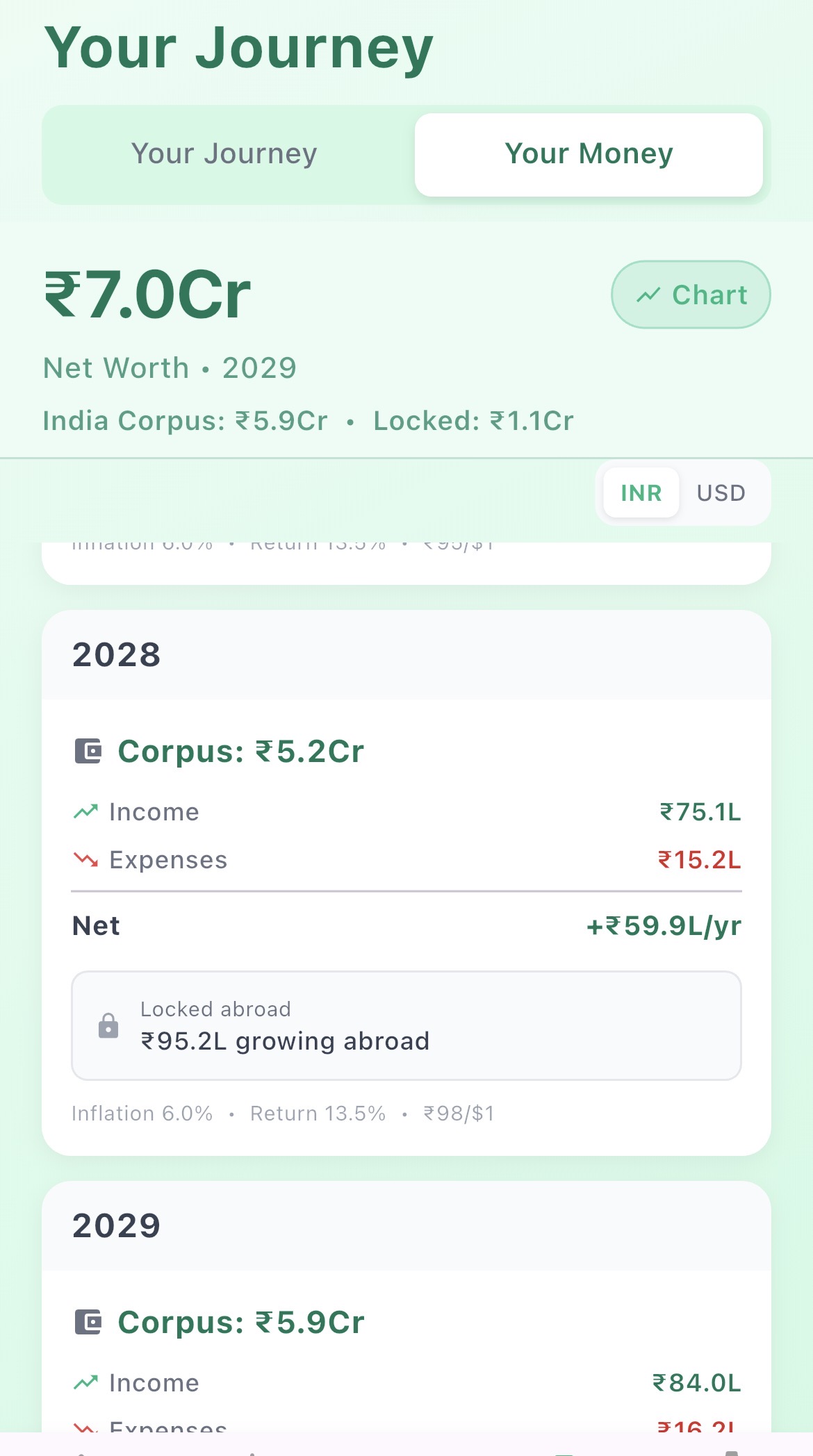

These scenarios are built on realistic assumptions: 6% corpus growth rate, 6% annual inflation in India, and corpus drawn down using a real-returns model. Use the Retire in India Calculator to build your own version.

Priya worked in IT in London for 22 years and built up a £350,000 SIPP plus 28 qualifying NI years. She retires to Pune at 50, owns a flat there, and will begin drawing UK State Pension (approximately £9,000/year — partial pension for 28 NI years) at 66.

Raj is a finance professional who wants to retire at 45 to Bangalore. He has £500,000 in a SIPP and ISA combined, but has only 18 NI qualifying years and won't receive a meaningful State Pension for 21 years. He needs the corpus to last until 72 without any pension income.

Anita and Suresh, both 55, return to Kochi after 30 years in the UK. Combined SIPP and DB pension pot of £600,000, plus Anita qualifies for £8,000/year partial State Pension starting at 66. They own a home in Kochi purchased five years ago. This is the scenario most UK NRI couples in professional roles can aspire to.

The difference between these scenarios comes down to three levers: retirement age, monthly spend, and whether State Pension income materially reduces corpus drawdown. The Retire in India Calculator lets you adjust all three in real time and see your personalised outcome.

The India-UK tax relationship is governed by the India-UK Double Taxation Agreement (DTA), which has been in place since 1993. Understanding how it applies to your specific income sources is essential — and the rules differ depending on what type of income you're receiving.

UK pension income (State Pension, workplace pension, SIPP drawdown) is generally taxable in the UK regardless of where you live. HMRC will apply UK income tax via PAYE on your pension payments. The India-UK DTA provides that pension income is taxed in the country of source — meaning the UK taxes it, and India does not tax it again. You should register with HMRC as a non-resident and have your UK bank account reflect your Indian address to ensure the correct tax code is applied.

When you return to India after being an NRI for many years, you typically qualify for Resident but Not Ordinarily Resident (RNOR) status for the first 2–3 financial years. During the RNOR period, foreign income (income earned outside India, including UK pension income received into a UK account) is generally not taxable in India. This provides a useful transition window to restructure your finances before full Indian residency tax rules apply.

After the RNOR period, as a full Indian resident, your worldwide income is technically taxable in India — but the DTA prevents double taxation by allowing a tax credit for UK taxes already paid on UK-sourced income.

UK ISA accounts lose their UK tax-free status once you become a non-resident — you can't contribute to them, and any income generated within the ISA may be taxable in India once your RNOR period ends. However, existing ISA balances can be retained in the UK and drawn down as needed. Many NRIs keep their ISA investments in UK equity funds and transfer proceeds to India gradually.

For a more complete view of the financial planning steps involved in an UK-to-India move, read our Return to India Financial Planning Guide. If you're also comparing your situation to NRIs coming from the USA, see our Retiring in India From the USA guide — the tax rules differ significantly.

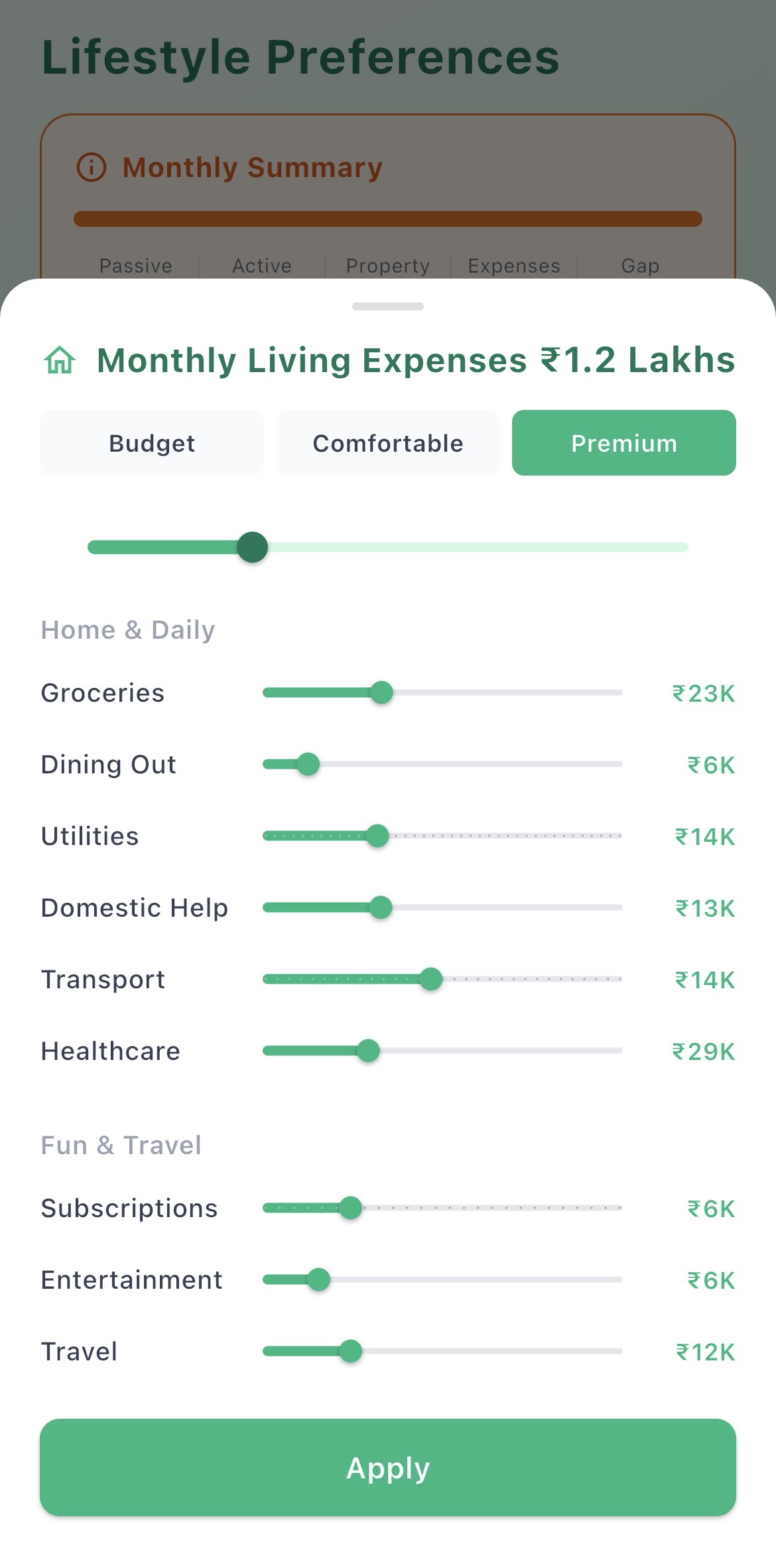

The honest answer depends on your lifestyle, city, whether you own property, and whether you have UK pension income supplementing your savings. But here are realistic benchmarks:

This only works if you also have a meaningful UK State Pension (35 qualifying NI years, full £11,502/year) starting at 66, you own a home in India, and you're willing to live in a Tier 2 city like Indore, Coimbatore, Mysore, or Nagpur. Monthly spend in this scenario: ₹70,000–₹90,000. This is a bare-bones retirement — manageable, but with very little financial buffer.

This is the range where retirement in a metro city (Bangalore, Pune, Hyderabad, Chennai) or a premium Tier 2 city becomes genuinely comfortable. With a partial or full State Pension kicking in at 66, you can spend ₹1,20,000–₹1,60,000/month and maintain a good NRI lifestyle — eating out, travel within India, good healthcare, and some international trips. This is the most common target range for UK NRIs in their 50s.

To understand what ₹3–4 Crore actually delivers in practice, see our detailed guides on whether ₹3 Crore is enough to retire in India and whether ₹5 Crore is enough.

At this level, you can retire to any major Indian metro, spend ₹2,00,000–₹3,00,000/month, travel internationally, support family members, and still have the corpus grow in real terms. This is the territory for UK NRIs who've had strong careers in finance, tech leadership, or medicine. See our Can You Retire in India With $1 Million? guide for what the upper end of this range looks like.

City choice is one of the most powerful variables in the UK NRI retirement equation. Retiring to Kochi or Coimbatore instead of Bangalore or Mumbai can extend your corpus by 5–10 years at the same spend level. Our guide to the best cities to retire in India covers the full comparison including healthcare quality, cost of living, and NRI community presence.

For a side-by-side comparison with NRIs coming from North America, see our Retiring in India From Canada guide — the CAD-INR dynamics and pension system are quite different from the UK, but the city choices and lifestyle considerations are similar.

Enter your GBP savings, UK pension income, city preference, and target spend — and see your full retirement projection.

Model your GBP corpus, UK pension income, city preference, and spend — and see your full 20-year financial projection.