Model your Canada-to-India retirement in Breather

Enter your CAD savings, CPP and OAS pension amounts, city preference, and target spend — and see your full retirement projection.

Canada's CPP and OAS pensions are paid globally for life — including in India — and together they can deliver ₹96,000–₹1,28,000/month before you touch a rupee of your savings. Here's exactly what Canadian NRIs need to know to make the numbers work.

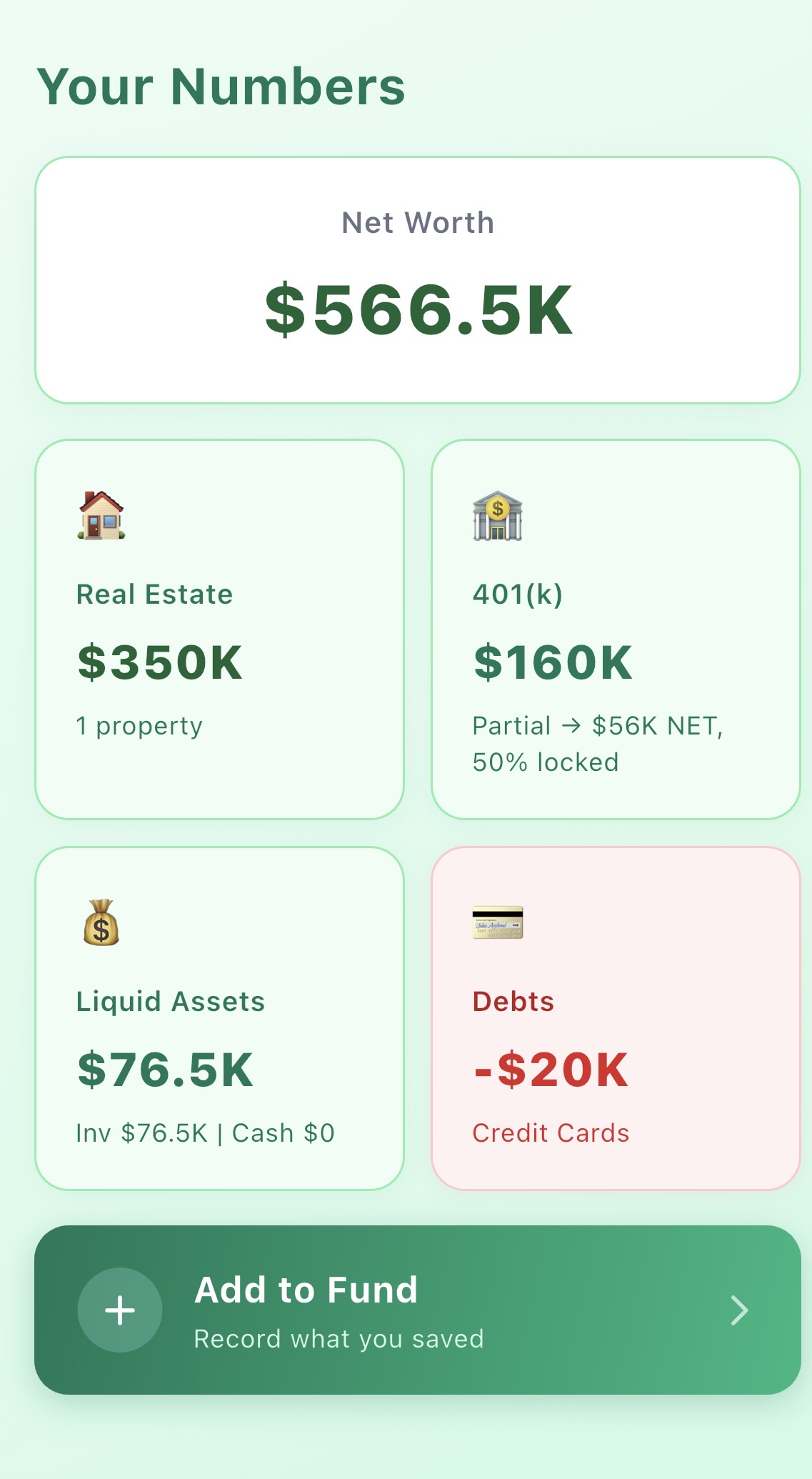

For Canadian NRIs, India is one of the most financially compelling retirement destinations in the world. At approximately C$1 = ₹64, a Canadian dollar buys a lot of comfort in India. A C$600,000 corpus converts to roughly ₹3.84 Crore — meaningful money that can fund a comfortable Indian retirement. But the real power of a Canada-to-India retirement comes from adding CPP and OAS pension income on top of that corpus.

Canada's retirement income system is considerably more generous than many NRIs appreciate. CPP (Canada Pension Plan) and OAS (Old Age Security) together can deliver C$1,500–C$2,000/month — that's ₹96,000–₹1,28,000/month — in guaranteed, inflation-indexed income for life. If you own a home in India, this pension income alone may cover your basic living costs entirely. Your corpus then becomes a buffer for healthcare, travel, and lifestyle upgrades rather than a monthly lifeline.

This fundamentally changes the retirement equation compared to NRIs from countries without strong social security systems. Use the Retire in India Calculator to model your specific CPP+OAS income against your target monthly spend and see how much corpus you actually need.

Many Canadian-Indian professionals in tech, healthcare, engineering, and finance have accumulated C$500,000–C$1,000,000+ in RRSPs, TFSAs, employer pensions, and non-registered investments. The key questions are:

For the foundational corpus analysis, see our guide on how much money you need to retire in India.

This is the most important section for most Canadian NRIs, and the one with the most upside. Both CPP and OAS are payable globally — you continue receiving them in India for life.

CPP is an earnings-based contributory pension. The average CPP retirement pension is approximately C$800/month (₹51,200/month), and the maximum for 2025 is C$1,306/month (₹83,584/month). You can start CPP as early as 60 (at a reduced rate) or as late as 70 (at an enhanced rate — 42% more than at 65). There is no Canadian residency requirement to receive CPP — it's based on your contributions, not where you live.

CPP is paid in CAD and can be received via direct deposit to a Canadian bank account, then transferred to your Indian NRE account. Service Canada also offers direct international transfers to certain countries including India through Global Affairs arrangements.

OAS is a residency-based pension — you qualify based on years of legal residence in Canada, not contributions. The basic OAS amount for 2025 is approximately C$700/month (₹44,800/month) at age 65. To receive OAS outside Canada, you must have lived in Canada for at least 20 years after age 18. If you have 20+ years of residence, you receive OAS indefinitely, even after moving to India permanently.

If you have fewer than 20 years of Canadian residence, OAS payments stop when you leave Canada (though you can receive them temporarily if you have at least 10 years). This is an important threshold — Canadian NRIs with 18 years of residence may want to consider staying an extra couple of years to cross the 20-year threshold before returning to India.

A Canadian NRI with a full career in Canada receiving both maximum CPP (C$1,306) and full OAS (C$700) would get C$2,006/month — approximately ₹1,28,384/month. Even at average CPP plus full OAS (C$800 + C$700 = C$1,500/month), that's ₹96,000/month in guaranteed, inflation-indexed lifetime income. If you own your home in India, this pension income alone may cover 80–100% of your monthly expenses in most Tier 2 cities.

RRSP (Registered Retirement Savings Plan) is Canada's primary tax-advantaged retirement savings vehicle — the rough equivalent of a US 401k. When you become a non-resident of Canada, the RRSP rules change significantly and tax planning becomes critical.

When you withdraw from your RRSP as a Canadian non-resident, the CRA imposes a non-resident withholding tax. For lump-sum withdrawals, this is 25%. However, under the Canada-India Tax Treaty, periodic RRSP payments (structured as regular drawdowns rather than one-time withdrawals) are taxed at a reduced rate of 15%. This distinction matters enormously — the difference between 15% and 25% on a C$500,000 RRSP is C$50,000.

Structuring your RRSP drawdown as periodic (monthly or quarterly) payments rather than lump sums is generally the more tax-efficient approach for Canadian NRIs. Work with a tax adviser who understands both the Canada-India treaty and CRA non-resident rules before making withdrawals.

All RRSPs must be converted to a RRIF (Registered Retirement Income Fund) or annuity by December 31 of the year you turn 71. RRIF withdrawals are mandatory at minimum amounts set by CRA each year. As a non-resident, these mandatory RRIF withdrawals are also subject to withholding tax. Planning for this mandatory conversion — especially if you move to India in your 50s — is important.

If you're planning your move and have 2–5 years before leaving, consider a pre-departure RRSP strategy: gradually withdraw from your RRSP in low-income years before leaving, paying Canadian income tax at lower marginal rates while you're still a Canadian resident. This converts taxable RRSP assets into after-tax cash that can then be invested in a TFSA or non-registered account — and ultimately transferred to India without further Canadian withholding.

TFSA (Tax-Free Savings Account) is the most NRI-friendly Canadian account. Withdrawals are always tax-free regardless of your residency status — there is no Canadian withholding tax on TFSA withdrawals. If you have TFSA assets, withdraw them before leaving Canada (while still a resident) to have clean, unencumbered cash to bring to India. Note: you cannot contribute to a TFSA once you become a non-resident.

For a complete view of financial planning considerations when returning to India, read our Return to India Financial Planning Guide.

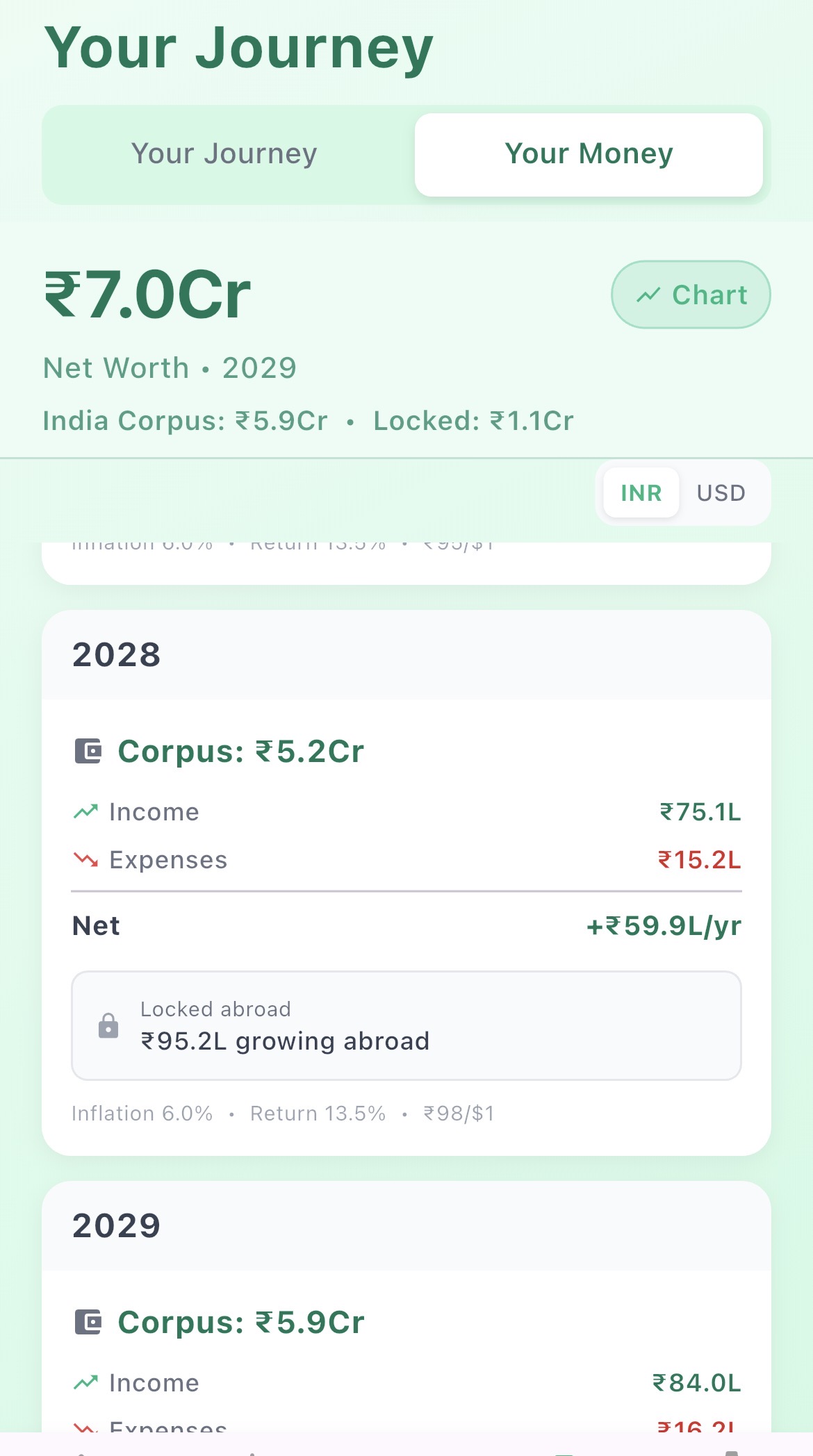

These scenarios use realistic assumptions: 6% corpus growth, 6% Indian inflation, and CPP/OAS treated as guaranteed fixed income starting at their respective ages. Run your specific numbers in the Retire in India Calculator.

Vikram, 55, worked in software engineering in Toronto for 28 years. He has C$400,000 in RRSP and non-registered accounts, full CPP entitlement (C$1,100/month starting at 65), and OAS at 65 (C$700/month — 28 years residence, qualifies for overseas payment). He retires to Pune where he already owns an apartment.

Meena, 48, is a doctor who wants to retire early and return to Bangalore. She has C$600,000 in RRSP and TFSA, but CPP won't kick in until she's 65 (17 years away) and OAS at 65. She's renting in Bangalore. No India property yet. She needs the corpus to last through the pre-pension bridge period without exhausting itself.

Arun and Deepa, both 60, return to Kochi after 32 years in Vancouver. Combined RRSP and non-registered savings of C$800,000. Arun receives full CPP of C$1,200/month at 65; Deepa C$900/month. Both qualify for OAS at 65 (C$700 each = C$1,400/month combined). They own a home in Kochi. At 65, their combined pension income is C$3,500/month = ₹2,24,000/month.

The pattern across all three scenarios is clear: the closer you are to CPP and OAS eligibility when you retire to India, the smaller the corpus you need. Early retirees (40s) need a substantially larger corpus to bridge the pension gap. The Retire in India Calculator models this bridge period automatically based on your age, target retirement date, and estimated CPP/OAS amounts.

Leaving Canada for good involves a clear tax residency break — and getting this right from day one saves significant money. Canada taxes residents on worldwide income, so staying technically resident while living in India would expose your Indian income to Canadian tax. The goal is to cleanly sever Canadian tax residency.

CRA determines tax residency based on your residential ties to Canada. To sever tax residency cleanly, you generally need to:

Filing the departure return is mandatory. It triggers a "deemed disposition" — CRA treats you as having sold most of your assets at fair market value on the date you left Canada. This can trigger capital gains tax on unrealised gains in your non-registered investments. Careful pre-departure planning (realising losses, timing of the move) can minimise this impact.

Once you've severed Canadian tax residency, any Canadian-source income (RRSP withdrawals, CPP, OAS, rental income from Canadian property, dividends from Canadian corporations) is subject to non-resident withholding tax. The Canada-India tax treaty reduces withholding on many income types: CPP and OAS are taxed at 25% (no treaty reduction for government pensions), while RRSP periodic payments are reduced to 15% under the treaty.

When you arrive in India after a long NRI period, you typically qualify for Resident but Not Ordinarily Resident (RNOR) status for the first 2–3 financial years. During RNOR, foreign income — including Canadian pension income received into a Canadian account — is generally not taxable in India. This transition window is valuable: you can let your Canadian accounts settle, manage RRSP withdrawals strategically, and reorganise your assets before full Indian residency tax rules apply.

After the RNOR period, as a full Indian resident, worldwide income is in principle taxable in India. The India-Canada Double Taxation Agreement prevents double taxation — Canadian withholding tax paid on CPP, RRSP withdrawals, and other Canadian income can be claimed as a credit against any Indian tax owed on the same income.

For a broader overview of the financial planning steps involved in returning to India from any country, read our Return to India Financial Planning Guide.

The answer is highly dependent on how much CPP and OAS you'll receive — and when. That said, here are realistic benchmarks based on common Canadian NRI situations.

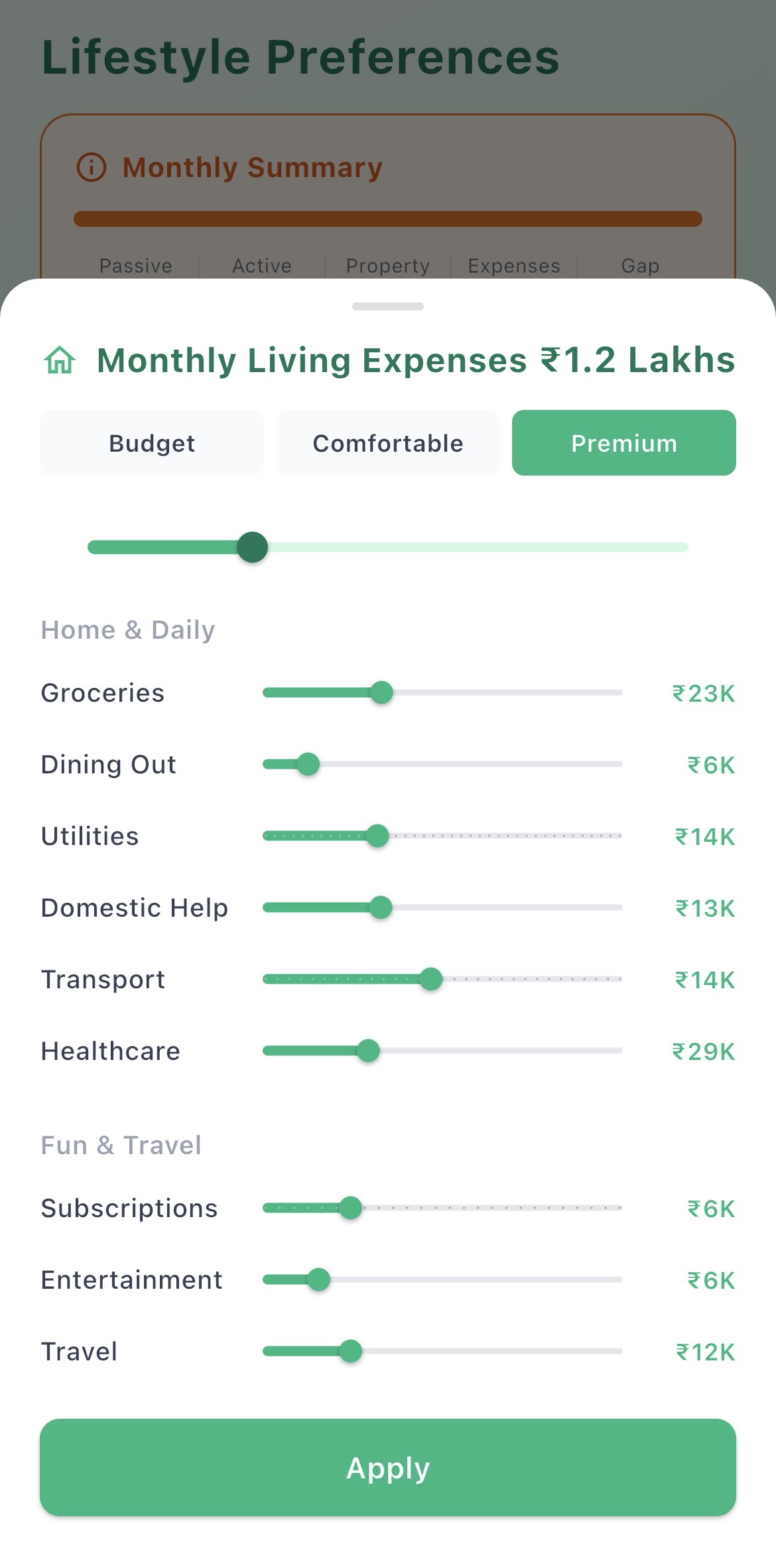

This only makes sense if you have full CPP and OAS entitlement (C$1,500–C$2,000/month combined) starting at 65 or earlier, you own your home in India, and you're retiring in a Tier 2 city like Coimbatore, Mysore, Nagpur, or Vizag. At this corpus level, the pension income does the heavy lifting and your savings serve as an emergency buffer. Monthly spend in this scenario: ₹70,000–₹1,00,000. This is a lean but liveable retirement for someone whose pension income is robust.

This is the sweet spot for most Canadian NRIs — enough to retire in a major metro (Bangalore, Pune, Hyderabad, Chennai), spend ₹1,20,000–₹1,80,000/month, and have the corpus bridge comfortably to CPP and OAS eligibility. If you're retiring in your mid-50s, this range gives you 10–15 years of comfortable drawdown before pension income covers most of your expenses. Our guide on whether ₹3 Crore is enough to retire in India walks through what ₹3.2 Crore (roughly C$500K) actually delivers month by month.

If you're retiring in your mid-40s, want to live in Bangalore or Mumbai with a premium lifestyle, or want to maintain international travel and support family members financially, you need C$700,000 or more. At this level, the corpus generates enough return to cover lifestyle expenses for 15–20 years before pension income arrives, and you maintain a meaningful financial cushion throughout. For what a very large corpus looks like in India, see our Can You Retire in India With $1 Million? guide — C$1 million is approximately equivalent to USD $730K at current exchange rates.

The city you choose to retire to is one of the most powerful variables in the Canadian NRI retirement equation. The cost of living difference between Bangalore and Kochi, or between Mumbai and Coimbatore, is significant enough to add 8–12 years to your corpus runway at the same spend level. Our detailed best cities to retire in India guide covers cost of living, healthcare quality, infrastructure, and NRI community presence for each major option.

For a comparison with NRIs returning from other countries, our Retiring in India From the UK guide covers how the GBP-INR dynamic and UK pension system differ from the Canadian picture. And if you want to compare with the US-India retirement path, see our Retiring in India From the USA guide — the Social Security system and 401k rules differ meaningfully from CPP/OAS and RRSP.

Enter your CAD savings, CPP and OAS pension amounts, city preference, and target spend — and see your full retirement projection.

Model your CAD corpus, CPP and OAS income, city choice, and monthly spend — and see exactly how your money lasts in India.