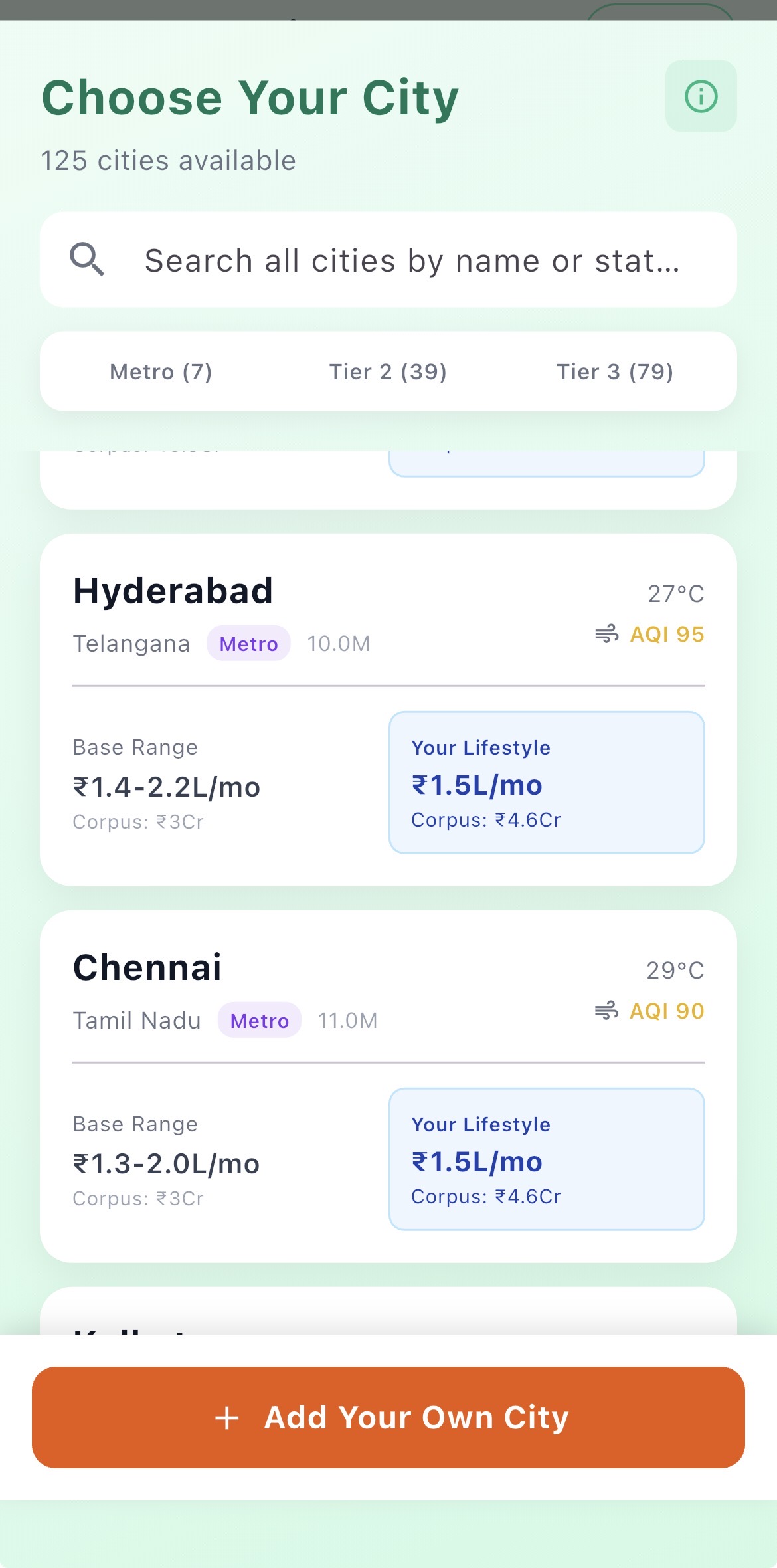

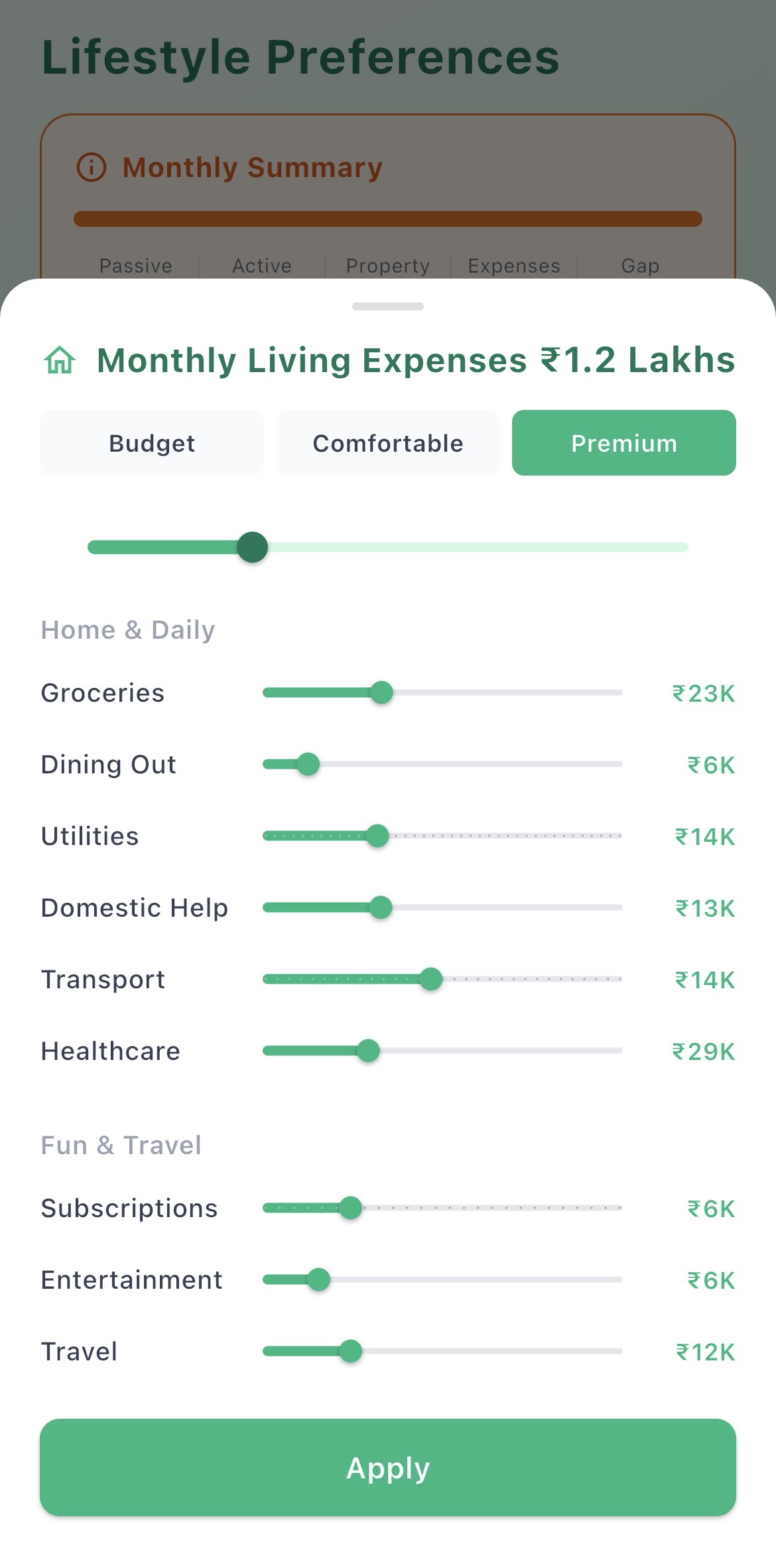

Model your India lifestyle costs in Breather

Enter your target city and lifestyle — and see exactly what it costs per month in India.

For NRIs planning a return, the cost difference between the US and India is the most important number in the retirement equation. Here's the real side-by-side breakdown — housing, food, healthcare, school, and transport — in both rupees and US dollars.

The short answer: for most NRI families, India is 3–5x cheaper than a comparable US lifestyle. But the multiplier varies dramatically by expense category:

The categories where India is not dramatically cheaper: imported goods, international travel, luxury brands, and certain categories of electronics. NRIs who maintain frequent US travel or an international lifestyle don't save as much as those who adapt fully to Indian living.

These figures are for a family of 3–4 (couple + 1–2 kids). US figures are for a mid-tier metro (Austin, Raleigh, Phoenix). India figures use Bangalore metro and Pune Tier 2 as two reference points.

| Expense | USA (Mid Metro) | Bangalore | Pune / Tier 2 |

|---|---|---|---|

| Housing (rent) | $2,800–4,000/mo | ₹50–80K/mo ($600–950) | ₹25–45K/mo ($300–540) |

| Groceries | $800–1,200/mo | ₹15–25K/mo ($180–300) | ₹10–18K/mo ($120–215) |

| Eating out | $600–1,000/mo | ₹10–20K/mo ($120–240) | ₹6–12K/mo ($70–145) |

| Private school (per child) | $1,000–2,500/mo | ₹15–40K/mo ($180–475) | ₹8–20K/mo ($95–240) |

| Healthcare (family insurance) | $1,500–2,500/mo | ₹3–5K/mo ($35–60) | ₹2–4K/mo ($24–48) |

| Transport (car + fuel) | $700–1,100/mo | ₹15–25K/mo ($180–300) | ₹10–18K/mo ($120–215) |

| Utilities + internet | $250–400/mo | ₹5–9K/mo ($60–107) | ₹4–7K/mo ($48–83) |

| Domestic help | $1,500–3,000/mo | ₹8–15K/mo ($95–180) | ₹5–10K/mo ($60–120) |

| Total (family of 4) | $8,000–15,000/mo | ₹1.3–2.3L/mo ($1,550–2,740) | ₹80K–1.5L/mo ($950–1,790) |

The savings are dramatic. A family spending $12,000/month in the US can maintain a comparable lifestyle in Bangalore for ₹1.8–2L/month (~$2,150–2,380) — a 5x cost reduction. In a Tier 2 city, the same family can live on ₹1–1.4L/month.

Healthcare is where the India vs USA cost gap is most dramatic — and most consequential for retirement planning.

| Procedure / Service | USA (with insurance) | India (private hospital) | Savings |

|---|---|---|---|

| Annual family health insurance | $18,000–30,000/yr | ₹30,000–80,000/yr ($360–950) | 95%+ |

| Cardiac bypass surgery | $70,000–200,000 | ₹3–6L ($3,600–7,100) | 95%+ |

| Hip replacement | $32,000–45,000 | ₹2.5–4.5L ($2,975–5,350) | 90% |

| GP consultation | $150–350 | ₹400–1,200 ($5–15) | 95% |

| Specialist consultation | $300–800 | ₹1,000–3,000 ($12–36) | 95% |

| Dental crown | $1,000–1,800 | ₹8,000–20,000 ($95–240) | 85–90% |

Quality at top Indian private hospitals (Apollo, Fortis, Kokilaben, Manipal) is comparable to US standards for most procedures. Many US-trained doctors practice at these hospitals. For NRIs, this means healthcare is not a quality compromise — it's an enormous cost advantage.

For NRI families with school-age children, private schooling is often the second largest monthly expense after housing. The India vs US cost difference here is significant.

| School Type | USA (annual) | India Metro (annual) | India Tier 2 (annual) |

|---|---|---|---|

| Public school (K-12) | Free (via taxes) | ₹30,000–80,000 | ₹20,000–50,000 |

| Private CBSE/ICSE school | N/A | ₹1–4L/yr | ₹60K–2L/yr |

| International school (IB/IGCSE) | $15,000–35,000/yr | ₹4–12L/yr ($4,800–14,300) | ₹2.5–6L/yr ($2,975–7,150) |

| Engineering undergrad | $50,000–80,000/yr | ₹1–4L/yr IIT/NIT; ₹4–12L private | Similar to metro |

Even the most expensive Indian private schools cost 50–70% less than equivalent US private schools. For families with 2 children in school, the annual education savings alone can fund a significant portion of India living costs.

Beyond the direct comparisons, India's lower price level means your retirement corpus generates substantially more lifestyle than in the US.

A $500K corpus in the US at a 4% withdrawal rate generates $20,000/year ($1,667/month) — enough for a very modest lifestyle in most US cities. The same $500K in India generates ₹1.4L+/month at equivalent returns, which funds a comfortable upper-middle-class lifestyle in most Indian cities.

This purchasing power differential is the core reason many US NRIs with modest savings can retire far more comfortably in India than they ever could in the United States.

To decide which city offers the best quality of life for your corpus size, see our guide on where to retire in India for NRIs. For the corpus you'll need, see how much money you need to retire in India.

Enter your target city and lifestyle — and see exactly what it costs per month in India.

Enter your city and spending habits — Breather shows your monthly budget and how far your corpus goes.